Planning Your Finances After Divorce: Embracing a New Start

Divorce is one of the most emotionally charged and expensive life events many of us experience. The twists and turns of ending a long-term relationship affect not only your emotional wellbeing but also your financial future. It is common to feel overwhelmed by the sudden change, especially when responsibilities double and income often shrinks. Thankfully, with careful planning and a patient step-by-step approach, you can establish a secure financial base and gradually rebuild what you once had.

In this opinion editorial, we will explore a detailed roadmap for processing your new financial reality after a divorce. We will dive in to examine practical strategies, provide useful tips in bulleted lists and tables, and share honest insights from leading personal finance experts. Whether you are just starting the process or are in the midst of reorganizing your finances, this guide will help you find your way through these confusing bits, making the transition as smooth as possible.

Rebuilding Your Budget from Scratch

One of the most immediate and nerve-racking challenges following a divorce is redefining your budget. Your previous financial setup was designed for a dual income household, and suddenly, you are adjusting to the reality of one income or altered maintenance payments. The key to regaining control is to start from scratch—breaking down your new income, expenses, assets, and debts.

Assessing Your True Household Income

After a divorce, the first step is to calculate your real income. Many people mistakenly assume that splitting your income in half will keep your finances stable. However, the reality is more complicated due to the hidden complexities of additional living expenses. Below are crucial factors to consider when evaluating your income:

- Source of Income: Consider salary, freelance earnings, child support, or spousal support. Make a complete list of regular incoming funds.

- Tax Adjustments: Understand that changes in filing status may significantly affect the amount you take home after taxes.

- Unexpected Deductions: Some expenses, such as legal fees or tax penalties from asset transfers, could impact your take-home pay.

It is essential to get into the fine points of your finances by calculating the net income available for your new household. Taking into account these details early on can prevent surprises later, allowing you to manage your money more efficiently.

Tracking Your New Spending Patterns

In the months immediately following a divorce, your financial priorities might change drastically—even in ways that are a bit tricky to determine. The key is to track your expenses for 2 to 3 months to get a clearer picture of where your money actually goes. Below is a table outlining typical expense categories before and after divorce:

| Expense Category | Before Divorce | After Divorce |

|---|---|---|

| Housing | Shared mortgage or rent | Separate leases or mortgages often with higher collateral costs |

| Utilities | Split evenly between partners | Full responsibility falls on the individual |

| Childcare | Co-managed costs | Often increases as two households aim to maintain similar standards |

| Healthcare | Shared plans or employer-based benefits | If previously on a partner’s plan, additional premiums now apply |

| Insurance | Joint policies with favorable rates | Individual policies usually command higher rates |

Regrettably, divorcing couples often find that despite expecting to split costs down the middle, they end up shouldering more than half of the individual expenses. The little twists in budgeting can be downright overwhelming if not planned carefully.

Evaluating Assets and Debts Post-Divorce

One of the most nerve-racking parts of the divorce process is sorting out what you take home. Here are the essential factors to keep in mind:

- Asset Distribution: Review the settlement details, including retirement funds, real estate, and other investments. It is critical to understand your new asset base.

- Debts and Liabilities: Know which debts you are legally obligated to continue paying and which ones have been settled. Some derivatives of joint liabilities might carry unexpected costs.

- Tax Implications: Assets like property transfers and retirement funds often carry tax burdens that affect your overall financial health.

Many individuals realize only after the divorce that their wealth has not merely been halved – it has shrunk even further due to additional hidden costs. Being aware of every little detail now may save you from costly surprises later.

Immediate Financial Priorities in the First 30-60 Days

The first two months following a divorce are crucial for setting the stage for your long-term financial health. These early days, though filled with their own set of (sometimes intimidating) financial decisions, will determine your path to recovery. It is essential to tackle the following key actions immediately.

Updating Beneficiaries and Legal Documents

When marital ties are severed, many documents—such as retirement annuities, life insurance policies, or bank accounts—may still list your ex-spouse as the default beneficiary. Without these updates, you could unwittingly be leaving your future to chance. It’s critical to:

- Review and update all beneficiary designations on insurance, investment accounts, and other financial instruments.

- Consult with an estate planner or legal expert to ensure that your will accurately reflects your current situation and your desires for guardianship, especially if children are involved.

Taking the wheel of these changes early can help prevent any additional complications or unintended legal consequences down the road.

Establishing an Emergency Fund

One of the key safeguards to protect against those nerve-racking unexpected expenses is establishing an emergency fund. The financial shock following a divorce can be compounded by unforeseen costs like medical emergencies, car repairs, or sudden changes in child support payments. Experts suggest aiming for an emergency fund that covers 3-6 months of essential expenses. Consider these steps to build your emergency fund:

- Start Small: Even if you begin with modest contributions, consistency is critical.

- Avoid Withdrawals: Consider the fund untouchable except for true emergencies, ensuring that it grows steadily.

- Automate Savings: Set up an automatic transfer to a dedicated savings account to make saving habitual and effortless.

Allocating even a small percentage of your income into this fund in the early days of your post-divorce life can help buffer the impact of immediate financial challenges.

Reviewing and Adjusting Insurance Needs

If you were previously on your spouse’s insurance plan, the transition to getting your own cover can be both intimidating and time-sensitive. It is important to refigure your insurance needs by considering the following:

- Health Insurance: Research and enroll in a medical aid plan that suits your new lifestyle. Compare different policies to find one that covers your essential needs without breaking the bank.

- Car Insurance: With changes to your credit score or driving records, be sure to shop around for the best rates that reflect your current circumstances.

- Home and Property: As a new single individual, the policies protecting your home might need to be reassessed to ensure comprehensive coverage.

- Disability and Life Assurance: Consider safeguarding your income and future assets with proper life or disability insurance policies.

By reexamining these options, you can avoid potential gaps in coverage and ensure that you are financially insulated from further risk.

Checking Your Credit Report

One critical yet often overlooked step is verifying your credit report. A divorce can leave behind joint debts or even errors from accounts that should have been closed. To avoid any damaging surprises, these steps should be taken immediately:

- Obtain a current credit report from one or more reputable credit bureaus.

- Highlight any discrepancies, such as unknown accounts or errors, and dispute them with the appropriate organizations.

- Monitor your credit score regularly considering that joint debts may still impact your creditworthiness.

Detecting and resolving any issues early on can be the difference between establishing a secure post-divorce credit profile and facing setbacks down the line.

Deferring Major Financial Purchases

After a divorce, it is tempting to seek a fresh start by making significant purchases—be it a new home, car, or lavish lifestyle upgrades. However, the transition period is not the ideal time for large financial commitments. Instead:

- Delay major expenditures for at least a year or two until your finances are settled.

- Prioritize building savings and strengthening your financial foundation before venturing into large purchases.

- Consider the long-term implications and affordability of such investments during times of uncertain income.

By postponing big purchases, you protect yourself from additional financial pressure during an already challenging transitional period.

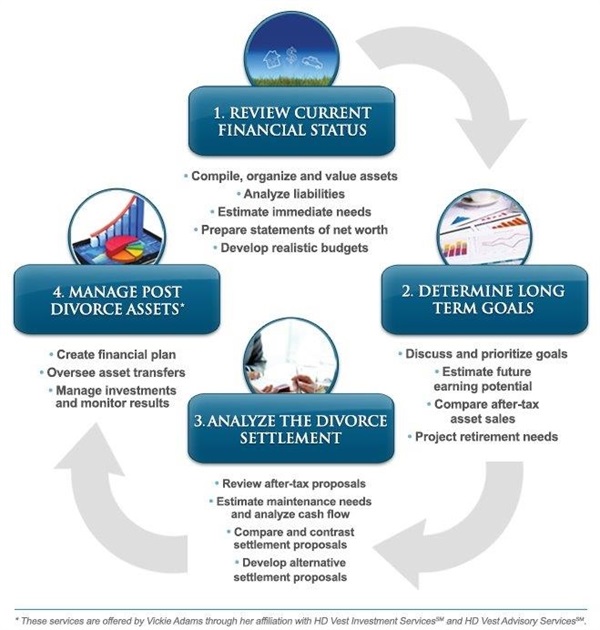

Long-Term Financial Strategies for Stability

Achieving long-term financial security post-divorce requires carefully recalibrating your financial goals. While the immediate post-divorce period focuses on urgent tasks, the following strategies are designed to ensure lasting financial resilience over the years ahead.

Revamping Your Retirement Planning

Divorce frequently disrupts your established retirement plans, especially if retirement funds were divided as part of the settlement. It is critical to:

- Assess Your Retirement Funds: Understand the amount that has been transferred or retained, and review the tax implications associated with these funds.

- Recalculate Savings Goals: With the knowledge that your post-divorce income may be lower, adjust your retirement contributions accordingly. Sometimes, revisiting previous lifestyle expectations and future needs is necessary.

- Consult a Financial Advisor: Professional guidance can help tailor plans that accommodate your new financial landscape and retirement goals.

Remember, it may take two to five years for your finances to fully stabilize post-divorce. Patience is essential as you adapt to new saving strategies and lifestyle adjustments.

Revising Your Will and Estate Planning

A divorce mandates a complete rework of your legal and estate documents. Not only does this involve updating beneficiary designations and property ownership details, but it also means revising your will and determining future arrangements for any children involved. Consider the following steps:

- Update Your Will: Ensure that your last wishes now truly reflect your current situation, eliminating any outdated references to your former spouse.

- Guardianship Arrangements: For parents, it is super important to review and adjust legal guardianship instructions so that they are aligned with your values and wish for your children’s future.

- Power of Attorney: Any legal powers granted to your ex-spouse need immediate attention and revision.

This process might seem laden with legal tangles, but sorting out these matters early helps prevent complications later on and offers peace of mind.

Meeting with a Professional Financial Advisor

Often, the additional challenge in working through your new financial life is knowing where to begin. While many divorcees attempt to figure a path on their own, collaboration with a trusted financial professional can make a significant difference. Consider these advantages:

- Personalised Advice: A seasoned financial advisor can help you analyze the subtle details of your financial situation and tailor a plan that works for you.

- Long-Term Roadmapping: Professionals can assist in crafting a strategy that includes saving for retirement, budgeting for daily expenses, and planning for unforeseen circumstances.

- Financial Discipline: Having an expert guide you through the fine points of budgeting and investments can help keep you on track during challenging periods.

Many individuals underestimate the benefits of professional guidance until the challenges become overwhelming. Getting professional advice early on might be the must-have step that ensures you do not stray from your financial goals.

Building a New Financial Identity

Beyond the numbers, divorce necessitates building a new financial identity—one that reflects your independent life and ambitions. This identity is shaped by not only the practicality of budgeting and savings but also by your ongoing personal goals. Consider these points:

- Personal Goal Setting: Write down both short-term and long-term financial goals. These could include goals like paying off debt, saving for a down payment, or starting an emergency fund. Use these lists as a motivational tool.

- Learning Financial Literacy: Invest time in understanding the little details of financial planning, from understanding interest rates to grasping subtle differences in various investment options. Webinars, podcasts, and online courses can be valuable resources.

- Adjusting Lifestyle Expectations: Recognize that the transition may require some lifestyle adjustments. It may feel off-putting at first, but gradually, learning to savor a simpler, yet more financially secure, lifestyle can be liberating.

Recasting yourself as the architect of your own financial future can bring a great sense of empowerment. It is essential to view this process as a unique opportunity rather than a setback, allowing you to rebuild your financial life in a sustainable and focused way.

The Role of Emotional Resilience in Financial Recovery

It is important to remember that the financial reorganization post-divorce is deeply intertwined with emotional recovery. Managing your money in the midst of personal upheaval might seem full of problems, but maintaining emotional stability directly influences your financial decision-making.

Coping Mechanisms for Stressful Transitions

Many people find the financial aspects of divorce distracting from the underlying emotional strains. Here are some strategies to help build resilience:

- Seek Professional Counseling: A mental health professional can help you manage the nerve-racking emotional shifts while you adjust to new financial responsibilities.

- Establish a Support Network: Join support groups or forums for divorcees. Sharing experiences can help alleviate the feeling of isolation and provide practical tips for both emotional and financial recovery.

- Practice Self-care: Ensuring you take time for yourself—not only enhances your emotional well-being but also sharpens your ability to make clear and effective financial decisions.

Understanding that financial issues are intertwined with emotional challenges can help you tackle both aspects with sensitivity and strength.

Balancing Immediate Needs with Future Goals

One common stumbling block for many post-divorce individuals is the continuous tug-of-war between immediate financial needs and long-term objectives. On one hand, the immediate tasks—from tracking expenses to updating legal documents—can feel all-consuming. On the other hand, setting future goals like retirement planning and home ownership is equally important.

Here are some strategies to manage this balance:

- Structured Planning: Create a calendar or digital planner outlining tasks for the first 60 days, ensuring you allocate time for both urgent and long-term financial planning.

- Regular Reviews: Schedule monthly financial check-ins to assess progress on immediate goals while simultaneously evaluating your long-term plan’s viability.

- Prioritization: Understand that some tasks require immediate attention while others can be planned incrementally. This balanced approach helps you manage your resources more efficiently.

By structuring your approach in both the short and long term, you can steadily work towards recovering financially without falling behind on essential everyday responsibilities.

Strategies to Recover Financially After a Demanding Divorce

As you emerge from a divorce, the financial challenges might appear overwhelming. Yet, many individuals have successfully rebuilt their lives by following key actionable strategies. Here, we offer a consolidated action plan to help you regain control over your finances.

Action Plan: Step-by-Step Guide

The following table lays out a comprehensive step-by-step action plan to guide you through the immediate and long-term phases of financial recovery:

| Step | Action | Timeline |

|---|---|---|

| 1 | Assess true household income including adjustment for new tax status. | Within first week |

| 2 | Track daily expenses to understand shifting spending patterns. | First 2-3 months |

| 3 | Update beneficiaries on all legal and financial documents. | First 30 days |

| 4 | Establish an emergency fund covering 3-6 months of essential expenses. | First 30-60 days |

| 5 | Review and update insurance policies to meet individual needs. | First 60 days |

| 6 | Check and correct your credit report for joint or unintended accounts. | First 30 days |

| 7 | Delay major expenditures until the financial foundation is restored. | First 1-2 years |

| 8 | Revise retirement plans and estate planning documents. | Within 6 months |

| 9 | Consult a professional financial advisor for tailored strategies. | Ongoing |

This detailed action plan provides an at-a-glance framework to help you stay organized during a period that might otherwise feel tangled with issues. The importance of each of these steps lies in their cumulative effect in rebuilding both your financial stability and personal confidence.

Embracing the New Financial Landscape With Confidence

Financial recovery following a divorce is neither immediate nor linear. It is a process that demands patience, daily commitment, and an ongoing willingness to adjust your plans. At times, the overlapping challenges may seem intimidating, but with persistence and careful strategy implementation, you can gradually build a stronger, more reliable financial future.

Collecting Lessons and Building Resilience

Divorce can be an opportunity to redefine not only your marital and personal life but also your financial identity. As you work through the many tricky parts—from assembling a new budget to managing long-term savings goals—stay mindful of the following key lessons:

- Adaptability: Financial strategies that worked in a dual-income household may not be efficient in your new setup. Remain flexible and be ready to revise plans as needed.

- Continuous Learning: As you dig into the little details of personal finance management, consider taking steps to enhance your financial literacy. This could include online courses, reading financial publications, or even attending financial planning seminars.

- Emotional Resilience: Recognize that the journey is as much about emotional recovery as it is about budgeting and asset management. Guard your mental and emotional health as you rebuild your life.

Every small step taken today forms the foundation for a more secure tomorrow. Keeping a positive outlook, while addressing financial responsibilities head-on, can transform what may feel like a period loaded with issues into a time of renewal and opportunity.

Final Thoughts: Patience, Professionalism, and Persistence

No matter how intertwined your personal and financial lives may have been, a divorce signals a chance to recalibrate and start anew. The transition involves handling numerous complicated pieces, and while the process is certainly nerve-racking at times, it also provides you with the chance to create a financial identity that is solely your own. The legal and financial advice offered here is intended as a guide to steer you through those unforeseen twists and turns ahead.

Remember, rebuilding from the ground up is not a sign of failure but one of reinvention. It requires the same level of care and often the help of professionals in both the legal and financial spheres. Keep in mind that while the journey may be long—often taking a few years to fully stabilize—each step you take is a key investment in a more secure and independent future. Stay positive, remain diligent, and gradually, you will find that what once seemed intimidating slowly evolves into a stable and fulfilling financial reality.

Conclusion: A Brighter Financial Future Awaits

Divorce often comes with an array of unexpected challenges—from recalibrating household income and budgeting afresh, to updating legal documents and safeguarding future investments. Navigating through these nerve-wracking changes requires a blend of immediate action, detailed long-term planning, and emotional resilience. This comprehensive guide has explored the must-have steps to tackle everything from updating beneficiaries to restructuring your retirement plans.

As daunting as the process may appear, every step you take is a step toward a new beginning. With resources, the support of experts, and a clear action plan, you are positioned to transform a difficult chapter into a time of personal and financial reinvention. Embrace the process, lean on professional support when needed, and gradually, you will build a future that reflects your newfound independence and strength.

Let this guide serve as both a roadmap and a reminder: every twist, every turn, and every challenging bit on this journey can eventually lead to a more resilient, confident, and financially secure you. A brighter financial future awaits—if you are willing to take that first decisive step.

Originally Post From https://www.primediaplus.com/2025/09/30/how-to-plan-your-finances-after-a-divorce-its-stressful-and-expensive

Read more about this topic at

Money and Divorce: 6 Financial Mistakes to Avoid

Financial Planning for a Divorce