Divorce Lending: A Growing Niche in Mortgage Planning

The mortgage industry is witnessing a significant shift as divorce becomes an increasingly influential factor in the way homeowners plan their finances. With rising property values, tighter lending guidelines, and a growing proportion of divorces among individuals in their 40s, 50s, and beyond, the financial world is forced to contend with a host of tricky parts that can affect both the lending process and the final outcome of a divorce decree.

Mortgage professionals are now facing tangled issues that arise from the intersection of family law and mortgage underwriting. This opinion editorial takes a closer look at the subtle details involved in divorce lending, discussing how the language of a divorce decree can have far-reaching consequences, and why early consultation is critical. The discussion also serves as a wake-up call to both legal and financial advisors who must work together to avoid costly mistakes and secure a stable financial future for their clients.

Understanding the Tricky Parts of Divorce Lending

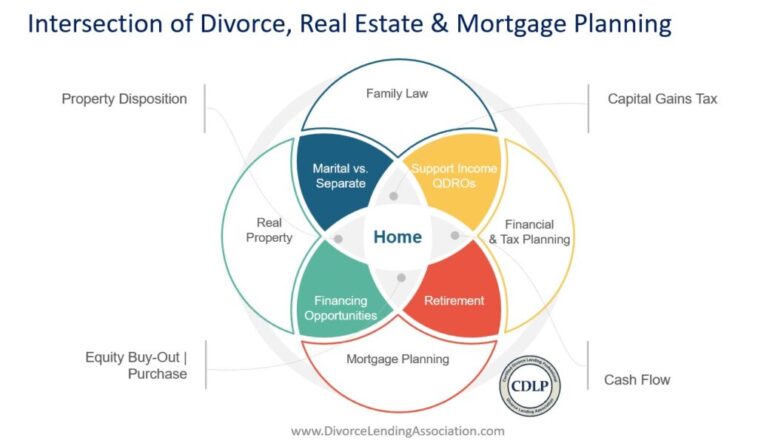

Divorce lending is a specialized area in the mortgage world that focuses on aligning the legal aspects of divorce, particularly the division of assets and declarations of income, with the strict guidelines imposed by lenders. This process involves several confusing bits and little details that, if not carefully considered, can reclassify a mortgage loan or even disqualify a borrower from obtaining desirable rates.

One of the most critical issues lies in the precise wording used in a divorce decree. Even the seemingly benign choice between terms such as “alimony” and “spousal maintenance” can determine whether support payments are considered qualifying income by institutions like the FHA. Similarly, misstatements concerning the division of equity in marital property can lead to unintended consequences, including the reclassification of the mortgage as a cash-out refinance instead of an equity buyout. Such reclassifications often bring with them less favorable loan-to-value ratios and higher interest rates.

Key Risk Areas in Divorce Decrees

To better understand the challenges, it helps to break down the risk areas associated with divorce decrees in mortgage transactions. Here are some of the most common areas of concern:

- Equity Division Missteps: Improperly detailing how property is divided can have lasting consequences on a homeowner’s ability to secure financing.

- Income Documentation: The fine points of how spousal support is listed may determine its acceptance as qualifying income for mortgage purposes.

- Loan Reclassification: Drafting errors can inadvertently change the nature of the transaction, turning an equity buyout into a cash-out refinance, which typically comes with tougher lending standards.

- Tighter Lending Guidelines: Lenders have become more cautious, and missteps in a divorce decree might result in delayed closings or even disqualification from attractive rates.

Each of these areas contains hidden complexities that require not only the expertise of a skilled attorney but also the strategic insight of a knowledgeable mortgage professional.

Getting Into the Fine Points of Dividing Property and Income

One of the most nerve-racking aspects of divorce lending lies in the way property and income are split. Given that a divorce decree must simultaneously satisfy legal requirements and mortgage underwriting standards, the wording chosen in these documents is of super important consequence.

Equity Division: Often, the central source of confusion is how equity in marital property is divided. If a decree labels a particular payout incorrectly, it might trigger stricter loan-to-value limits, resulting in increased interest rates. The decree needs to clearly distinguish between what constitutes a buyout and what might be seen as cash extraction from the property. Failing to maintain that clarity may significantly jeopardize a client’s financial standing during a stressful transitional period.

Income Declarations: Similarly, the fine points surrounding income declarations can be tricky. Mortgage professionals require that support payments not only be documented clearly but also projected to continue for a minimum period—often at least three years. This requirement ensures that borrowers have a reliable income stream to support future mortgage obligations.

Consider the following table, which outlines the critical language differences and their potential impacts:

| Description | Term Used | Potential Impact on Mortgage Qualification |

|---|---|---|

| Ongoing Support | Alimony | May be accepted if structured correctly, but often subject to change based on the divorce settlement |

| Monthly Payment Requirement | Spousal Maintenance | Clearly documented as ongoing support, increasing chances of being considered qualifying income |

| Equity Payout Classification | Buyout vs. Cash-Out Refinance | Misclassification can lead to unfavorable lending conditions or disqualification |

This table serves as a reminder that even the slight differences in language can have a ripple effect on lending options. Mortgage professionals must, therefore, get into the nitty-gritty of every contract point to protect the financial interests of their clients.

Early Consultation: Don’t Wait Until After the Decree Is Signed

One of the most common missteps observed in the handling of divorce lending cases is the delay in consulting a mortgage specialist until after the divorce decree is finalized. At that late stage, it is often too late to adjust the language or structure of the agreement to secure the best possible mortgage options.

It is super important for borrowers—and the professionals involved—to engage with a mortgage expert early on. By involving a specialist during the negotiation of the divorce decree, both parties stand much better chances of structuring financial arrangements that are both legally sound and acceptable to lending institutions.

Early engagement allows for:

- Reviewing Draft Decrees: Mortgage professionals can review draft documents to point out risky sections before they become final.

- Collaborative Input: The combined expertise of legal and financial consultants ensures that the language used is beneficial, or at least not detrimental, to future financing needs.

- Future-Proofing Agreements: Proper consultations enable homeowners to keep future lending options open by avoiding labels or structures that would automatically trigger more stringent loan conditions.

When mortgage experts and legal professionals work together during the divorce process, they can formulate strategies that steer through the tricky parts of property division and income documentation, creating a more secure financial path moving forward.

Collaboration Between Lenders, Attorneys, and Financial Planners

The transition of personal finances during a divorce is not a solo challenge—it is one that requires a team of professionals. The collaboration between lenders, family law attorneys, and financial planners has become an essential part of modern divorce strategies. When all parties are on the same page, the potential for miscommunication decreases dramatically, and both parties can achieve a fair and sustainable financial outcome.

Below is a bulleted list summarizing the benefits of interdisciplinary collaboration:

- Better Communication: Regular interactions between parties help ensure that everyone understands the objectives and limitations of the agreement.

- Integrated Financial Planning: Professionals can combine insights from different fields, making it easier to foresee long-term financial consequences and to mitigate risks early.

- Increased Flexibility: With the combined knowledge of mortgage guidelines and legal requirements, solutions can be tailored to fit the unique circumstances of each case.

- Smoother Execution: A well-coordinated plan reduces delays in the mortgage approval process and minimizes the chance of post-decree disputes.

This trend underscores the notion that handling divorce lending is less about isolated decision-making and more about crafting a comprehensive financial strategy that holds up under both legal scrutiny and the rigorous demands of mortgage underwriting.

Tackling the Confusing Bits of Financial Coordination in Divorce

Divorce is, on its face, a deeply personal experience. However, when significant assets like a family home are involved, the decisions made can have long-lasting financial implications. Mortgage professionals, in particular, face the challenge of balancing the urgent emotional needs of their clients with the practical demands of financial stability.

The sudden financial independence of divorcing homeowners often means that previously shared financial responsibilities must be reevaluated and restructured. In these situations, even the small distinctions in wording can lead to major shifts in mortgage eligibility and interest rates. For example, if income from support payments is not documented over a long enough period, it may not be considered stable enough by a lender, thereby affecting the client’s ability to secure favorable mortgage terms.

Mortgage professionals must therefore help guide homeowners through these tangled issues, ensuring that every element—be it equity division or income documentation—is handled with precision and foresight.

Specialized Approaches for Silver Divorces

In recent years, an increasing number of clients divorcing later in life have presented with a unique set of challenges. Often referred to as “silver divorces,” these cases tend to involve multiple properties, retirement accounts, and a more intricate web of financial commitments. Here, the stakes are even higher: the financial missteps in property division or support agreements can jeopardize decades of financial planning.

A seasoned mortgage professional must be able to take a closer look at these scenarios and provide a coordinated plan that addresses both the current and future financial needs of their clients. This involves:

- Evaluating multiple income streams and the stability of each over the long term

- Reassessing property values to ensure that each party maintains a fair share of equity

- Reviewing retirement and investment portfolios to ascertain their impact on mortgage qualifications

With the right preparation and expert guidance, homeowners can steer through the confusing bits of post-divorce planning without sacrificing their future financial stability. The goal is to provide a seamless transition that preserves equity and maintains access to competitive mortgage rates, even in the midst of significant personal change.

Strategies to Avoid Costly Mistakes During Divorce Lending

One of the super important lessons that both mortgage professionals and divorcing homeowners have learned is that preventive planning is key. Waiting until after a divorce decree is finalized to consult a mortgage expert can close off numerous opportunities that might have otherwise existed with proper forethought.

Here are several strategies that can help prevent the most common and expensive mistakes in divorce lending:

- Proactive Document Reviews: Engage with both legal and financial advisors during the drafting stage of a divorce decree to flag any problematic language that could affect mortgage eligibility.

- Clear Role Distribution: Establish who is responsible for reviewing financial documents and ensure that mortgage professionals have full visibility over pertinent sections of the divorce agreement.

- Future-Proof Agreements: Draft decrees with provisions that allow for adjustments in the future to accommodate changing financial circumstances, such as shifts in income or property values.

- Regular Updates: Stay informed about evolving lending guidelines which may affect divorce lending cases, ensuring that any advice given is up-to-date and comprehensive.

These preventive measures are not just about avoiding pitfalls; they are about constructing a financial bridge that leads to long-term stability and growth, even after life-altering events like divorce.

Practical Guidelines for Mortgage Professionals

For mortgage professionals, understanding the safe path through divorce lending is an exercise in both legal expertise and financial strategy. The role of a Certified Divorce Lending Professional is super important: they are specially trained to get around the tangled issues that arise from the merging of divorce law and mortgage underwriting.

Consider the following practical guidelines that mortgage experts can adopt when working with divorcing clients:

- Early Engagement: Initiate conversations with clients as soon as divorce discussions surface. Early planning allows for modification of agreements before they become unchangeable.

- Detailed Document Analysis: Scrutinize divorce decrees to identify and rectify any problematic language or classifications that may impact mortgage terms.

- Collaboration with Legal Experts: Foster a strong working relationship with divorce attorneys who understand the financial stakes of property division and support agreements.

- Continual Education: Stay updated on the latest lending criteria and regulatory changes that might impact divorce lending practices.

- Client Education: Make sure that clients are fully aware of the subtle parts of their divorce documents that may be overlooked but have significant financial impact.

By following these guidelines, mortgage professionals enhance their ability to offer high-value advice that minimizes risk and maximizes the potential for favorable mortgage terms even in the midst of significant personal upheaval.

Future-Proofing Mortgage Strategies in Divorce Situations

It is clear that divorce lending is loaded with problems that can derail even the best-laid financial plans. However, with proactive measures and the right expert guidance, many of these issues can be managed effectively. The key is to ensure that all parties involved—from the divorcing couple to their legal advisors and financial experts—understand the rate of change in both market and legal standards.

Planning ahead is more than a precaution; it is a strategy designed to prevent future disputes. For couples, regardless of marital status, drafting agreements that detail how equity will be handled in the event of major life changes can be a lifesaver. This allows both parties to have a clear understanding of their financial rights and responsibilities, reducing the potential for tension and misunderstandings later on.

Mortgage professionals can encourage couples to set up detailed agreements that point out the small distinctions in financial contributions and expectations. Whether the couple is unmarried or married, having clear documentation and strategies in place can ease the process of securing a mortgage and ensure a smoother transition if circumstances change radically. Such foresight is critical, especially given that life’s twists and turns rarely follow a predictable path.

Assessing and Managing Risk in Divorce Lending Transactions

While divorce lending carries its share of challenges, it also presents opportunities for those who are prepared to work through the nerve-racking details. Risk in these transactions is not solely about the language in the divorce decree; it also involves the timing, the coordination among specialists, and the overall market conditions.

Risk management in divorce lending can be approached from several angles:

- Legal Risk: Ensuring that the language used in divorce decrees is precise and aligned with mortgage underwriting requirements. This reduces potential legal disputes down the line.

- Financial Risk: Addressing risks such as fluctuating property values and income instability by incorporating flexible clauses in mortgage agreements.

- Operational Risk: Managing the timing of consultations with mortgage experts to avoid delays in the loan process.

By identifying each component of risk, mortgage professionals and legal advisors can better direct their resources and expertise to mitigate potential pitfalls. This structured approach not only helps to find your way through the challenging bits of a divorce lending case but also instills confidence among all parties involved.

Innovative Approaches in Modern Divorce Lending

As market demands evolve and consumer expectations shift, the world of divorce lending is expected to continue changing rapidly. Innovative strategies are emerging as mortgage professionals leverage technology and new communication channels to better serve their clients. Digital tools allow for real-time collaboration between legal advisors, financial planners, and mortgage experts, ensuring that every decision made during the divorce process is documented and accessible.

Some of these innovative approaches include:

- Online Document Sharing: Secure platforms that enable all parties to review, comment, and update divorce decrees and financial documents.

- Virtual Consultations: Timely discussions via video conferencing that help expedite the review process, even if all parties are not physically located in the same area.

- Automated Alerts: Software that flags potential issues in language or classifications within the decree before final submission.

These digital solutions not only help mortgage professionals work through the small distinctions and hidden complexities of divorce lending but also allow for a more transparent and collaborative process. The role of technology in streamlining these operations further reinforces the importance of early and collaborative planning in today’s dynamic economic environment.

Financial Stability and Mortgage Security After Divorce

The overarching goal in any divorce lending scenario is to pave the way for financial stability for both parties. Securing a mortgage that reflects a fair assessment of the borrower’s financial condition is paramount during these transitions. A well-structured divorce decree, coupled with proactive consultation, can significantly enhance a client’s ability to secure favorable mortgage terms and preserve substantial property equity.

Here are some key takeaways for achieving mortgage security post-divorce:

- Clear and Consistent Documentation: Ensure that every relevant detail in the divorce decree is documented in a way that meets lender standards.

- Regular Financial Reviews: Update financial plans periodically to reflect changes in income, property value, and market conditions.

- Collaborative Approach: Involve all relevant professionals early in the process to protect both parties’ interests.

- Adaptive Financial Planning: Develop a flexible strategy that can adjust to life’s sudden shifts, protecting long-term goals even when circumstances change.

These measures underscore the idea that sound mortgage planning in the context of divorce is not merely about meeting the technical requirements of a lender—it’s about building a sustainable foundation for the future. When homeowners are equipped with the right financial tools and expert guidance, they are better positioned to transform a stressful transition into a manageable, even positive, turning point in their lives.

Conclusion: Securing Your Financial Future Through Effective Divorce Lending Strategies

Divorce lending is a specialized and challenging field within the broader mortgage industry. The process is scattered with nerve-racking twists and turns that demand careful attention to detail and early intervention. With clear documentation, proactive planning, and interdisciplinary collaboration, the risks associated with the fine details of divorce decrees can be effectively managed.

Professionals in both the legal and mortgage arenas must take a proactive role in managing these challenging bits—from understanding the subtle parts of property division to getting into the nitty-gritty of qualifying income requirements. The advent of new technology and digital communication tools further empowers professionals to work through the tangled issues quickly and efficiently, ensuring that both parties retain their financial stability during and after the divorce process.

Ultimately, effective divorce lending strategies go beyond simple compliance with underwriting guidelines. They represent a commitment to designing a financial future that is robust, flexible, and fair—one that acknowledges the reality of life’s changes while providing a clear path forward. In an era when personal and financial landscapes are evolving at an unprecedented pace, the thoughtful planning afforded by early consultations and cross-disciplinary cooperation stands out as a key driver of long-term mortgage security.

Whether you are a homeowner facing a challenging divorce or a professional tasked with guiding clients through these nerve-racking processes, it is incumbent upon all parties to recognize the super important need for attention to detail. By carefully managing the problematic language in divorce agreements and ensuring that every financial decision is made in close collaboration with experts, individuals can secure the support they need—the right mortgage terms, competitive interest rates, and above all, a stable financial future on the other side of divorce.

In conclusion, divorce lending might be full of problems and loaded with tension, but with the right strategy and teamwork, it can be transformed from a potential minefield into an opportunity for financial renewal. With clear communication, innovative technological solutions, and a commitment to proactive planning, both professionals and clients can ensure that divorce becomes not an end, but a new beginning marked by economic resilience and stability.

Additional Considerations for Divorcing Homeowners and Professionals

For those engaged in the divorce process, several additional considerations can help ensure that the mortgage remains a tool for building future wealth rather than a source of additional stress. The following bullet list highlights some practical steps:

- Maintain Open Communication: Keep regular contact with all your advisors to ensure that everyone is updated with new developments and any changes within the divorce decree.

- Keep Detailed Records: Save all correspondence and documents related to the divorce and mortgage application. This establishes a strong paper trail that can help clarify details in case of discrepancies later.

- Reassess Financial Goals: Divorce often triggers a reevaluation of long-term financial objectives. Ensure that your new mortgage plan aligns with your adjusted goals.

- Review Legal Terms Thoroughly: Ask your attorney to explain every little twist and detail that might impact how your divorce decree is interpreted by lenders.

- Consider Mediation: Mediation can be an effective way to resolve disputes in a collaborative setting, ensuring that both parties’ financial interests are considered.

By following these additional steps, homeowners and professionals alike can work together to minimize risks and maximize the benefits of a well-managed divorce lending strategy.

Final Thoughts: A Collaborative Path Forward

Divorce lending represents one of the more challenging intersections of law and finance. However, with the right mix of early planning, interdisciplinary collaboration, and attention to the smallest details, the pitfalls that once loomed large can be neutralized. Rather than becoming overwhelmed by the confusing bits and nerve-racking twists of divorce decrees, both homeowners and professionals now have access to strategies and tools that help them sort out the hidden complexities of their financial arrangements.

As we look to the future, it is clear that the marriage between legal expertise and mortgage planning will only grow stronger. The ultimate benefit of this partnership is the protection of homeowners’ interests—and the preservation of financial stability during one of life’s most challenging transitions. In an environment where every detail matters, proactive consultation and a strategic approach will remain key factors in turning a tense transition into a well-managed financial journey.

In a world where divorce and its financial implications are becoming ever more intertwined, the expertise of a dedicated mortgage professional, in tandem with a knowledgeable legal advisor, is not just an advantage—it is a necessity. With careful planning, a commitment to clear and precise documentation, and an unyielding willingness to collaborate, both parties can secure a path that leads to lasting financial stability and future prosperity.

Ultimately, the lessons learned from divorce lending are universal: clear communication, early engagement, and relentless attention to the fine points are key to not only surviving but thriving in the wake of personal upheaval. Whether planning for the future, reassessing a financial stance after divorce, or simply trying to secure a competitive mortgage rate, understanding and managing these tricky parts can make all the difference. It is, therefore, imperative that all involved take the time needed to map out their strategies carefully—because the road to financial security, though sometimes filled with nerve-racking challenges, can indeed lead to a more stable, hopeful future.

Originally Post From https://www.mpamag.com/us/mortgage-industry/industry-trends/divorce-lending-what-brokers-need-to-know/554711

Read more about this topic at

Divorce Lending Association – Expert Divorce Mortgage …

Divorce lending: What brokers need to know