Understanding the Rising Trend of Gray Divorce

The phenomenon known as “gray divorce,” referring to the dissolution of marriages among individuals aged 50 and above, has been subtly reshaping the landscape of family law and social norms in America. While overall divorce rates have fallen since their peak in the 1980s, recent data shows that a growing number of baby boomers are choosing to end their marital relationships later in life. This development has significant implications for retirement planning, financial security, and even legal frameworks designed to protect both spouses. In this opinion editorial, we will get into the many angles and tangled issues of gray divorce—from the shifting dynamics of long-term relationships to the ever-more intricate interplay between personal choices and broader social trends.

Historical Shifts and Data Insights on Late-Life Divorces

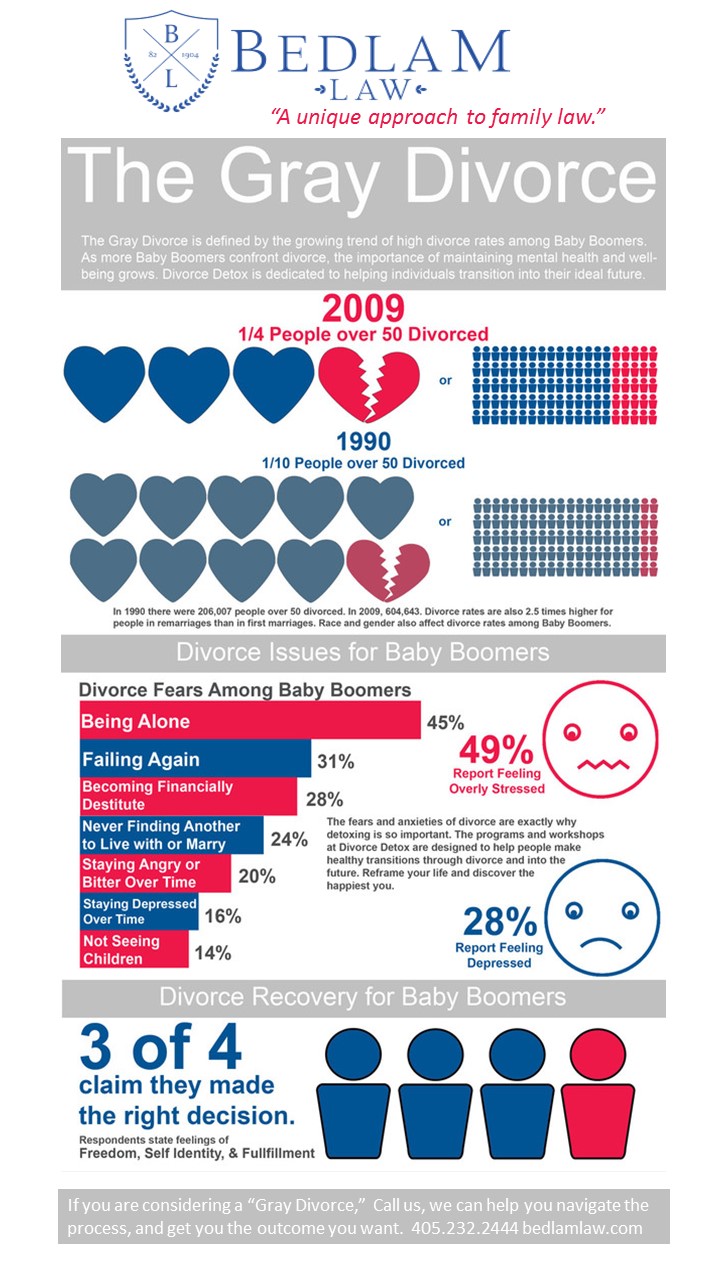

An analysis of federal data by the Pew Research Center reveals that the so-called “gray divorce” rate has sharply increased over the past few decades. In 1990, the divorce rate among married women aged 50 and older was approximately 3.9 per 1,000. By 2008, that figure had jumped to 11, and in 2023 it was documented as 10.3 divorces per 1,000 married women in that age group. This upward trend stands in stark contrast to the overall divorce rate, which has dropped from a peak of 22.6 divorces per 1,000 married women in 1980 to 14.4 in 2023.

The refined divorce rate—a metric that divides the number of divorces by the number of married women aged 15 and older, then multiplies the outcome by 1,000—offers a more accurate picture of these changes. Such a measure is particularly helpful because it accounts for shifts in marriage rates that have occurred over the decades. Whereas the divorce rate for individuals aged 15 to 49 remained relatively stable from 1990 to 2008 at about 28 divorces per 1,000 married women, it plummeted to 19.6 divorces by 2023.

This clear divergence between the trends in gray divorce and the overall divorce statistics raises several questions. What are the factors behind this rise in late-life marital separations, and what does it mean for individuals on the brink of or already entering retirement? As we take a closer look at these statistics, it becomes evident that longer life expectancies and evolving social attitudes have played a key role in redefining what it means to remain married in later life.

Demographic Transitions and Longer Life Expectancies

One of the most critical factors attributed to the increase in gray divorce is the dramatic rise in life expectancy. Today, individuals in their 50s and 60s can often anticipate another two or more decades of life—a prospect that shifts how couples evaluate their long-term compatibility. When someone is 65 and expects to live another 20 years, spending those extra years in an unfulfilling or even tense marriage can seem like an overwhelming prospect.

Several experts have noted that the longer lifespan means that many marriages may simply outlive their original purpose. Whereas in previous generations a spouse’s death might have been the primary method of “exiting” a long-term relationship, modern couples now face the possibility of decades together if the marriage continues. This prolonged timeframe accentuates the importance of evaluating whether the relationship still provides emotional, social, and financial benefits.

- Increased longevity provides more time for personal growth and change.

- Longer lifespans mean that the consequences of a poor marital relationship are experienced over a more extended period.

- Retirement planning and financial decisions become more complicated when factoring in the prospect of several more decades together.

Finances and the Tangled Issues of Retirement Security

Divorce, regardless of age, often triggers a series of tricky parts from both a legal and financial perspective. For older adults, separating a life built over many decades requires dividing assets, re-evaluating retirement plans, and sometimes even adjusting living arrangements. With the rise of gray divorce, these complicated pieces of separation stand to significantly affect not only the individuals directly involved but also the broader economy as retirees face potential financial instability.

Financial planners and legal experts have highlighted several key considerations for those contemplating divorce in later life:

- Retirement Savings: Splitting retirement accounts, pensions, or other savings can lead to reduced financial security in the latter years of life.

- Housing Arrangements: Many older couples may have shared homes built over decades. Deciding who stays and how to fairly handle the property distribution is often nerve-racking.

- Social Security Distribution: Adjustments in Social Security benefits and other entitlements can lead to long-term financial consequences.

- Healthcare Costs: As individuals age, healthcare becomes more critical, and managing these costs after a divorce can be scary.

| Aspect | Pre-Divorce Considerations | Post-Divorce Challenges |

|---|---|---|

| Retirement Savings | Jointly managed funds and shared assets | Equitable division and potential reduction in retirement funds |

| Housing | Shared property with historical sentimental value | Deciding on occupancy, refinancing, or selling triggering emotional and financial strain |

| Social Security | Combined benefits and collaborative retirement strategies | Reevaluation of benefits and potential loss of spousal benefits |

| Healthcare | Joint insurance plans and dual eligibility benefits | Effectively managing single-income healthcare expenses |

Late-Life Separation: Social and Emotional Considerations

The decision to end a long-term marriage is rarely driven solely by financial factors. Social and emotional elements also play a crucial role in what many call the “gray divorce revolution.” Recent sociological research indicates that beyond economics, individual happiness and personal fulfillment are influencing these decisions.

In earlier decades, divorce was often stigmatized, with many couples remaining together despite a relationship that had grown tense or full of problems. Today’s society, however, is more accepting of personal reinvention—even in later life—leading many older couples to break free from marriages that no longer provide the comfort and companionship they once did. For many baby boomers, the opportunity to spend additional life years pursuing personal goals, hobbies, or new relationships is seen as a refreshing prospect rather than a risky gamble.

Notably, the decision to separate later in life is often accompanied by an understanding that love, respect, and mutual support can take on different forms over time. Legal professionals note that while children were once seen as the strongest reason to hold on to an unhappy marriage, today’s older couples often find that children serve as a delay rather than a comprehensive deterrent to divorce. The emotional landscape in gray divorce scenarios is complex and filled with many little twists, from managing extended family dynamics to recalibrating social circles.

Expert Opinions on Baby Boomer Divorce Dynamics

Legal scholars and sociologists alike point to the unique characteristics of the baby boomer generation when explaining the upsurge in gray divorce. Professors such as Susan Brown and I-Fen Lin have documented what they refer to as the “gray divorce revolution.” Their research highlights that while only a small fraction of divorces in the 1970s and 1980s occurred among those aged 50 and older, the percentage has climbed significantly over time. In 2010, about one-quarter of all divorces involved individuals over 50, and by 2019, this rate had risen to 36 percent.

Andrew Cherlin, a professor emeritus of policy, has emphasized that the current pattern of gray divorce is largely the result of the baby boomers—the very generation that helped spark the divorce revolution in their youth—entering older adulthood. He suggests that as these baby boomers eventually pass on, the trend might level off. Until then, however, legal frameworks and social institutions must adapt to manage the outcomes of these separations.

Jennifer Glass, a sociology professor, adds another layer to the discussion by noting that older individuals are often more financially secure than previous generations. With greater independence comes the nerve-racking reality that many older adults can maintain separate lifestyles comfortably, even after decades of marriage. This financial independence, combined with the ability to lead fairly separate lives once the children have grown up and left home, makes divorce a more palpable option.

Credit, Care, and Legal Frameworks in Modern Gray Divorces

As divorce rates change within the golden years, legal professionals find themselves tasked with managing the fine points of asset division, credit issues, and long-term care planning. The process is loaded with issues that stray far from the simpler separations of younger couples, and the need to dig into these financial documents becomes particularly tricky when relations have spanned multiple decades.

Legal experts advise that understanding the subtle details of grey divorce requires not only a command of family law but also an appreciation for the many changes in personal circumstances that occur in later life. It is super important to consider:

- Asset Division: Older couples often possess significant marketable assets, real estate, and other investments. Dividing these items equitably can be nerve-racking and requires a structured approach.

- Credit Histories: Over the years, married couples might have jointly accumulated debts or built separate credit profiles, which need careful evaluation during divorce.

- Pension and Retirement Funds: With decades of joint contributions, pensions and retirement accounts present a significant and delicate challenge during asset division.

- Long-Term Care Planning: Considering that healthcare needs increase with age, plans need to be adjusted to accommodate future care expenses, both for each individual and any shared insurance benefits.

Attorneys often underscore the importance of approaching these separating matters as an opportunity to figure a path that respects the long shared history while preparing both parties for a future that might be filled with more separate achievements. It is this balance—dividing the past while protecting individual futures—that lies at the heart of modern gray divorce legal proceedings.

Steps to Ensure a Fair and Equitable Separation

For couples facing gray divorce, experts recommend several practical strategies to help manage both the financial and emotional toll of the process:

- Legal and Financial Counseling: Secure advisors who specialize in late-life divorces and understand the complicated pieces that come with decades of shared assets.

- Transparent Financial Disclosures: Ensure that all financial documents, debts, and assets are thoroughly disclosed to avoid any nerve-racking surprises later in the process.

- Mediation Services: Engage a mediator who can help both parties get around the challenging bits by working through the detailed negotiation of assets and future responsibilities.

- Retirement Planning Adjustments: Consult retirement planners to rework financial forecasts that take into account the re-sharing of assets and possible changes in income sources.

- Emotional Support: Access counseling services or support groups that can help manage the personal and relational stress inherent in late-life separations.

These steps are designed not just to ensure a fair distribution of tangible assets but also to help both parties discover a way to manage their way through the process with as little additional tension as possible. In each case, the goal is to make a nerve-racking decision as smooth and equitable as circumstances will allow.

Personal Reflections on the Changing Face of Marriage in Later Life

As an observer of legal trends and societal shifts, the phenomenon of gray divorce invites us to reflect deeply on how personal relationships evolve with time. Marriages that once seemed set in stone are now subject to re-examination as individuals continue to grow and change long after the wedding day. For many, the decision to separate is a reminder that the pursuit of personal happiness can sometimes outweigh the desire to cling to familiar routines. This sentiment is underscored by the fact that many older individuals are now in a position to steer through complicated relationship dynamics and prioritize their own well-being.

Some argue that our society’s acceptance of divorce, particularly in later life, is a sign of evolving norms as well as increasing individualism. Decades ago, the twist and turns associated with ending a long-term union would have been considered off-putting. Today, however, the conversation has shifted from one of stigma to one of practical concern: How do we ensure that both parties can continue to thrive independently after separating? This rethinking of traditional marriage roles is having a profound impact not only on personal lives but also on legal policies crafted to guide the dissolution of these unions.

The shift is perhaps most visible in how financial planning and legal oversight are conducted. While once the primary focus might have been merely on ending the marriage, now there exists a dual emphasis on sustaining individual financial security and paving the way for future personal development. This evolution is reflected in both legislative debates and judicial decisions related to asset division, spousal support, and retirement benefits. In many ways, the gray divorce trend is as much a story about modern economics as it is about love and companionship.

Repercussions for Retirement and Future Financial Planning

The reality of gray divorce brings with it a cascade of practical concerns that extend well beyond the personal realm and into the broader spectrum of retirement and economic security. As many divorce cases among older adults unfold, experts note that a divorce can lead to considerable changes in how retirement funds and pensions are allocated. Financial forecasting must now account for the fact that assets, once jointly held, need to be divided in a manner that supports two independent retirement plans.

This situation is complicated further by the fact that older adults may have accumulated wealth over many decades. The division of property, investments, and other assets can present a series of fine shades, each of which might significantly alter the long-term financial landscape for those involved. The consequences of not planning adequately can be nerve-racking, as reduced financial security in retirement may lead to increased reliance on state or federal assistance programs.

In response to these challenges, experts advocate for thorough financial planning well in advance of any potential divorce. Legal and financial advisors recommend:

- Creating detailed inventories of all marital assets.

- Evaluating prospective future income streams and potential liabilities.

- Developing contingency plans for unexpected healthcare costs or changes in living arrangements.

The goal in all these cases is to ensure that, even after the legal separation, both parties are in a strong position to enjoy a financially stable and fulfilling retirement years. As such, managing your way through the fine points of the separation process can create a more secure future, even in the face of what might initially seem like nerve-racking challenges.

Policy Implications and Social Adaptations Amid Changing Trends

The rising tide of gray divorce also forces lawmakers, financial institutions, and social service providers to reimagine support structures for this demographic. From a legal standpoint, the steady rate of divorces among those aged 50 and older has prompted calls for updated guidelines that address everything from pension splits to asset division under the unique circumstances of a long-term, late-life marriage. Some legislative proposals suggest the need for standardized divorce mediation services tailored specifically for older adults, while others recommend enhanced counseling resources to support the emotional well-being of those undergoing the separation process.

Policy experts emphasize that, given the public nature of these changes, state and federal agencies must work proactively to manage the subtle details and tricky parts that accompany such major life transitions. Some of the policy areas under discussion include:

- Updating family law to reflect the unique financial and emotional needs of older divorcing couples.

- Providing tax incentives for equitable division of retirement funds and pensions.

- Offering educational programs aimed at guiding older adults through the complexities of financial independence after divorce.

- Ensuring adequate mental health support to help individuals transition through the social ramifications of gray divorce.

Such adaptations not only serve the immediate needs of those facing divorce, but also help create a legal and social framework that embraces the idea of reinventing personal identities later in life. In a broader sense, these changes mirror the evolving nature of society as individuals increasingly prioritize personal fulfillment—a perspective that is both progressive and accommodating of the challenges posed by modern longevity.

Facing the Future: Professional Guidance and Personal Empowerment in Gray Divorce

In the end, the wave of gray divorce is a reflection of changing values, shifting demographics, and the increasingly complex interplay between personal choice and economic necessity. Legal practitioners, financial planners, and social researchers all agree that while the decision to end a long-term relationship in later life is loaded with tense challenges, it also opens the door to new beginnings and personal growth.

For those who find themselves confronting the possibility of a late-life separation, it is essential to take proactive steps to ensure a smooth transition. This might involve:

- Seeking comprehensive legal advice to get around the intimidating legal bits of asset division and custody arrangements, if applicable.

- Working with financial advisors who can help rework retirement plans and forecast future financial stability.

- Engaging in counseling sessions to manage the emotional twists and turns that invariably accompany the end of a long-standing relationship.

- Connecting with support groups where the subtle details of gray divorce can be discussed in a respectful and understanding environment.

Finding your path through the complicated pieces of gray divorce requires both a clear understanding of the legal and financial systems and a readiness to embrace change. For many, the decision to divorce later in life is not taken lightly—it reflects a deep commitment to quality of life, even if it means confronting many nerve-racking challenges along the way.

Embracing New Opportunities: Redefining Life After Divorce

While separating after decades of marriage might initially seem off-putting, many individuals find that what follows is a period of significant personal reinvention. The idea of starting over later in life, once seen as a daunting prospect, is now part of a broader conversation about the value of personal happiness and the right to lead an independent life. Social attitudes have evolved, and many see gray divorce not only as an end but also as a new beginning that offers fresh opportunities in both social and professional realms.

With new experiences come new networks, hobbies, and even career opportunities, all of which may contribute to an individual’s overall well-being. Here are some ways in which embracing life after divorce can turn a period of transition into one of personal empowerment:

- Rediscovering Personal Interests: Many individuals use this time to dive in to hobbies and pursuits they might have postponed during their marriage.

- Strengthening Social Connections: Reconnecting with friends, family, and community groups can help rebuild personal support structures.

- Redefining Career Goals: For some, this phase marks an opportunity to explore new career avenues or entrepreneurial ventures.

- Enhancing Financial Literacy: Managing finances independently can foster a sense of accomplishment and self-reliance.

By taking control of their future after a gray divorce, individuals can gradually transition to a life that is not only financially secure but also emotionally rewarding. The careful balance of legal prudence, financial planning, and personal optimism can lead to a new chapter that respects the past while focusing on the many opportunities that lie ahead.

Concluding Thoughts: Balancing the Past with a Promising Future

The trends observed in gray divorce are emblematic of broader societal changes that call for both legal innovation and personal courage. As more baby boomers choose to separate later in life, the legal system, financial institutions, and society as a whole must figure a path that acknowledges the delicate balance between long-held commitments and the need for individual fulfillment. There is no single answer to the challenges posed by gray divorce; rather, it calls for a combination of enhanced legal frameworks, thoughtful financial planning, and, above all, personal empowerment.

In rethinking what it means to divorce in later life, we are forced to confront not only the tangled issues of asset division and retirement security but also the more subtle parts of human happiness and personal change. Each case of gray divorce is a reminder that a long-term relationship, no matter how rich in shared history, may eventually succumb to personal growth and the desire for a more satisfying life. As society continues to adapt to these shifting dynamics, the legal and financial communities have a super important role in ensuring that each individual is given the opportunity to manage their way confidently through life’s later turns.

Ultimately, the rise in gray divorce invites us all to reexamine the notion of lifelong commitment. It challenges the old idea that divorce is something that happens only in youth, suggesting instead that the calculus of marriage can change as we grow older. With longer lives come longer relationships—but also longer periods to explore happiness, adjust ambitions, and settle matters that once might have seemed overwhelming. Whether viewed from a legal, financial, or personal perspective, gray divorce represents both the end of a chapter and the beginning of a new narrative—one that is rich with potential for reinvention and growth.

As legal professionals and social observers, it is our responsibility to guide those facing these transitions by offering clear and empathetic advice. With proper planning, open dialogue, and the support of compassionate experts, individuals navigating a gray divorce can transform a nerve-racking experience into a journey of renewed self-determination and future promise. Just as life continually evolves, so too must the institutions and personal strategies that support us in our later years.

In conclusion, while gray divorce poses numerous challenges—from tough asset divisions and reconfigured retirement plans to the emotional toll of ending a long-standing relationship—it also underlines a crucial truth: that personal fulfillment and the right to a happy, secure future are worth advocating for at any stage of life. As our population ages and these trends become increasingly prevalent, both public policy and personal strategies must keep pace, guiding individuals with clear, supportive frameworks that acknowledge the subtle details of modern love and independence.

By embracing a balanced approach that respects the history of long-term commitment while also empowering individuals to pursue a more satisfying life, our society can ensure that the rises and falls of gray divorce ultimately contribute to a richer, more resilient future for everyone involved.

Originally Post From https://www.newsweek.com/gray-divorce-bucks-national-trend-10912806

Read more about this topic at

Rising Divorce Among Middle-Aged and Older Adults …

“Gray divorce” bucks national trend