Retirement Realities: The Gap Between Hope and Readiness

The latest report on retirement and healthcare costs reveals a concerning disconnect between how optimistic employees feel about their retirement and the practical steps they are taking to secure financial stability. While many workers express confidence thanks to strong social connections, hobbies, and a sense of purpose, the actual financial preparedness just isn’t keeping pace. This opinion piece aims to poke around the reasons behind this gap and to offer a critical look at what employers and advisers can do to help turn good intentions into workable plans.

It is clear that employees are struggling to find their way through the tricky parts of retirement planning. With rising inflation, persistent economic uncertainty, and unexpected healthcare costs looming on the horizon, many people find the task of preparing for the future both intimidating and overwhelming. Despite these nerve-racking challenges, few individuals are fully capitalizing on available tools like automatic escalation, catch-up contributions, and tax-advantaged retirement accounts that can help them steadily increase their savings over time.

Understanding Financial Wellness in a Changing Economy

One of the key findings in the report was that emotional optimism about retirement is not being matched by practical financial actions. Amid rising economic pressures, 43% of Americans are losing confidence in the overall economy, and 71% worry that inflation could slowly erode their hard-earned savings. This situation is further complicated by the fact that many employees aren’t making the necessary moves to safeguard their futures. Despite advances in market conditions, savings rates remain alarmingly low, leading to a gap that could leave many workers exposed to unexpected shocks in later life.

It is no secret that when you’re juggling the many tangled issues of everyday life—including rising living costs and unpredictable job markets—the urgent need for long-term planning can easily take a back seat. Many employees simply aren’t making the concrete decisions required to secure a stable retirement. A lack of written retirement plans, minimal consultation with financial advisers, and hesitancy to use employer-sponsored financial wellness programs have all contributed to this worrying trend.

Healthcare Preparedness: A Weak Link in Retirement Planning

One of the most alarming revelations in this report is the significant drop in healthcare readiness among workers. Achieving only 36.7% of their potential in planning for healthcare costs shows that many employees are unprepared to manage the frightening reality of rising medical expenses during retirement. From long-term care to surprise medical bills, the financial fallout from healthcare needs represents one of the most intimidating challenges workers will face.

A large number of employees remain unsure about coverage specifics, with widespread concern over Medicare’s future adequacy. Even as many consider their future emotional readiness to be high, the subtle details surrounding healthcare expenses continue to create an environment loaded with problems. If left unaddressed, these confusing bits will likely compound the financial strain experienced by many seniors.

Dissecting the Healthcare Conundrum

- Uncertainty Around Medicare: Many workers lack confidence in the future of government-provided healthcare, which fuels anxiety about potential out-of-pocket costs.

- Surprise Costs: The risk of sudden medical emergencies and the resulting bills can wreak havoc on retirement savings.

- Long-Term Care Needs: The increasing likelihood that more retirees will require prolonged medical or assisted living support magnifies the need for robust financial planning.

The findings indicate that while emotional resiliency remains high—implying workers feel mentally ready for retirement—the fine points of planning for healthcare are being overlooked. Without addressing these subtle parts, workers may face serious financial setbacks at the very stage when stability is most needed.

Policy Uncertainty and Market Instability: A Double-Edged Sword

Another dimension of the problem is the concern over economic and policy conditions. With consistent market volatility, ongoing inflation, and fears of changes in Social Security, employees find themselves on edge about the future. These uncertain conditions have led to a significant drop in policy-related confidence within the workforce.

The continual twists and turns of the market not only make it hard to plan effectively, but they also contribute to a pervasive sense of insecurity. Many workers are unsure how to optimize their retirement accounts in this climate, and the lack of proactive measures adds another layer of risk to their financial futures.

Economic Challenges: A Closer Look

Several key issues are at play when discussing the economic challenges impacting retirement planning:

- Inflation Influence: Rising prices make it increasingly difficult for workers to boost their retirement contributions—even if they intend to raise their savings over time.

- Market Volatility: A constantly shifting market environment often leaves employees hesitant to make long-term investments or adjustments to their portfolios.

- Policy Changes: Frequent changes in policies related to Social Security and healthcare result in an unpredictable environment that complicates financial planning efforts.

These factors create a labyrinth of issues and challenges that workers have to get around without clear guidance. With such an unpredictable backdrop, even a well-intentioned savings strategy can soon unravel under the pressure of unforeseen circumstances.

The Role of Employers in Bridging the Retirement Gap

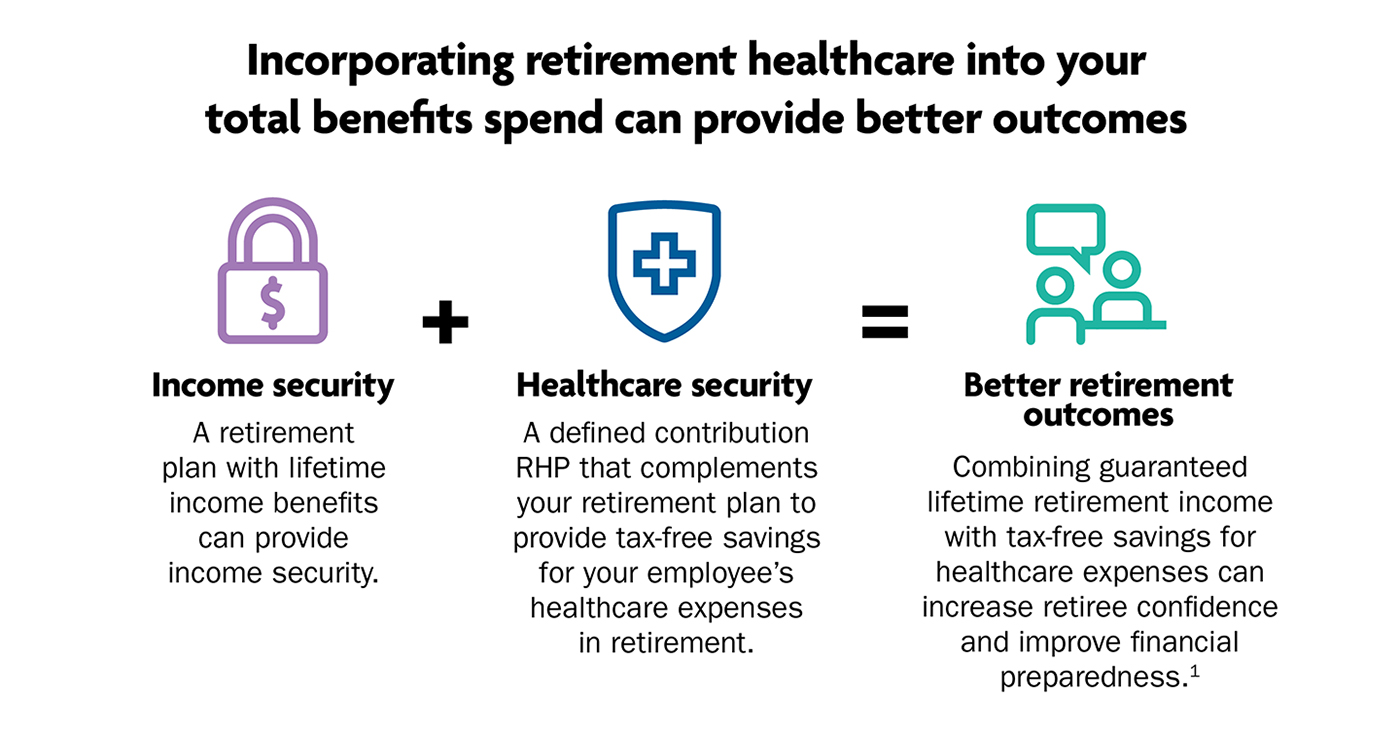

Given the significant gap between emotional readiness and practical financial planning, employers have a super important opportunity to make a meaningful impact. Employers can play a key role by enhancing benefit offerings that target both retirement savings and healthcare preparedness. By making financial wellness education and robust retirement planning a part of the regular workplace experience, companies can empower their employees to turn concern into concrete action.

One effective strategy is providing access to certified financial planners as a workplace benefit. This resource can help employees craft written retirement plans, set realistic savings goals, and optimize Social Security decisions. Furthermore, employers can support workers by aligning benefit programs with automatic contribution increases, catch-up contributions for those over 50, and tailored education around investment options.

Employer-Led Initiatives for Financial Wellness

Some of the initiatives that companies can consider include:

- Access to Certified Financial Advisors: Regular sessions or one-on-one consultations can help employees get into the nitty-gritty of financial planning.

- Retirement Planning Workshops: Hosting seminars that cover the small distinctions between different types of retirement accounts and saving strategies.

- Automatic Escalation Programs: Implementing systems where employee contributions increase automatically can help overcome the frustrating challenge of inflation eroding current savings.

- Healthcare Savings Accounts: Offering high-deductible health plans paired with Health Savings Accounts (HSAs) can provide a key financial buffer for medical expenses in retirement.

- Regular Communication: Sending timely updates about policy changes, contribution limits, and market trends helps employees stay informed about their financial health.

By taking such steps, employers can steer through the maze of unpredictable economic shifts and provide a more stable foundation for retirement planning. This not only benefits the individual employee but can also contribute to a more positive overall workplace culture and improved employee retention.

Practical Steps for Employees: Demystifying the Retirement Process

For many workers, the journey toward a secure retirement can feel riddled with tension and overwhelming challenges. However, adopting a clear, step-by-step approach can demystify those tricky parts. The key is to move from a passive state of emotional optimism to active, tangible actions that improve financial readiness.

Employees need to take a closer look at their existing financial strategies and identify areas for improvement. This means reevaluating current retirement accounts, setting up automatic contribution increases, and making full use of employer-provided planning resources. Beyond that, preparing for unexpected healthcare costs requires dedicated planning and the creation of specific strategies to manage these expenses.

Steps to Enhance Retirement Preparedness

Here are some actionable tips for employees who want to shore up their financial readiness:

- Create a Written Plan: Documenting a clear roadmap for retirement is a super important first step. This should include savings targets, timelines, and a breakdown of expected costs.

- Consult with Financial Advisers: Professional guidance can help get into the fine shades of planning that many workers overlook. A financial adviser can provide personalized advice that reflects individual circumstances and goals.

- Increase Contributions Gradually: Utilize employer features such as automatic escalation to steadily increase your retirement savings over time. This approach can help counteract the impacts of inflation.

- Plan for Healthcare Costs: Set aside dedicated funds or invest in HSAs to mitigate the risk of falling short when medical expenses strike. This is an excellent way to ensure that healthcare needs do not derail your retirement plan.

- Stay Informed: Keep up with changes in the economic landscape, policies affecting retirement and healthcare, and employer-provided benefits. Regular updates can help you adapt your strategy as circumstances evolve.

While the path to retirement security might seem tangled with confusing bits at first, adopting a proactive and informed approach can sharpen your focus. It’s all about transitioning from a state of worry to a state of strategic action.

The Importance of Timely Action in an Ever-Changing Landscape

At the heart of the problem lies the need for timely action. The longer employees delay concrete steps toward securing their retirement, the more exposed they become to the inevitable twists and turns of the economic landscape. Whether it is market volatility, inflationary pressures, or the rising cost of healthcare, each day that passes without a solid plan in place only increases the risk of financial instability.

In short, employees are at a crossroads between emotional readiness and the practical, sometimes complicated pieces of financial planning. The sooner workers can shift from an attitude of hopeful optimism to actionable planning, the better their chances will be of enjoying a secure and comfortable retirement.

Why Procrastination is Costly

Procrastination can have several consequences, including:

- Missed Opportunities: Early contributions and compounding interest are fundamentals that can make a huge difference. Delaying action means missing out on these advantages.

- Increased Financial Pressure: Postponing savings can lead to a sudden scramble later in life, which is often nerve-racking and stressful.

- Greater Impact of Inflation: With inflation continuously eating into savings, delaying contributions leaves workers more vulnerable to the slow erosion of their purchasing power.

The economic stage is set for significant changes ahead. With potential policy shifts and an ever-evolving market environment, every moment counts. Whether you are an employee or an employer, the time to act is now. Delaying strategic decisions today could result in a much tougher financial climb in the future.

The Employer’s Perspective: Creating a Culture of Financial Confidence

Employers stand in a unique position as sponsorships for financial literacy and long-term security. They have a super important role to play in helping employees find their way through the nerve-racking labyrinth of retirement planning. By integrating robust financial wellness programs within the workplace, companies can create a culture that not only values but actively promotes financial security.

For many employers, the initiative to offer financial wellness benefits goes beyond merely fulfilling a corporate social responsibility. It significantly influences overall workplace morale, retention of talent, and even productivity. When employees feel super important benefits have been thoughtfully designed to cover both retirement and healthcare costs, they are more likely to engage deeply with their long-term planning goals.

Key Components of a Financially Healthy Workplace

| Area of Focus | Example Initiatives | Potential Benefits |

|---|---|---|

| Retirement Planning | Automatic escalation of contributions, catch-up options, regular advisor sessions | Steady savings growth, better retirement outcomes |

| Healthcare Cost Management | High-deductible health plans paired with HSAs, wellness programs | Reduced out-of-pocket medical costs, increased preparedness |

| Financial Education | Retirement planning workshops, one-on-one financial advising | Greater financial literacy, empowered decision-making |

| Communication | Regular updates on benefits, market trends, and policy changes | Increased transparency and better strategic planning |

By instituting these programs, employers not only manage to cushion employees against the unpredictable shocks of the market but also foster an environment where financial confidence is not just encouraged but is woven into the fabric of the organization.

Turning Good Intentions Into Real Plans: The Way Forward

It is evident that while many employees remain mentally geared for retirement, their savings and preparedness still lag behind. This gap between emotional and practical readiness is not only a personal concern for the workers involved—it’s an issue that impacts the broader economy, the sustainability of social safety nets, and the overall stability of the workforce.

Both workers and employers must work together to bridge this divide. To this end, concrete actions must be taken:

- Enhanced Access to Financial Expertise: Employers should facilitate regular interactions with certified financial planners, ensuring that employees understand the fine shades and subtle details of creating a secure retirement plan.

- Comprehensive Benefits Packages: A restructured benefits package that explicitly focuses on both healthcare and retirement planning can help mitigate the risks posed by rising costs and policy uncertainties.

- Employee Education Programs: Regularly scheduled workshops and seminars can demystify the complicated pieces of financial planning, helping employees move from emotional readiness to actionable steps.

- Technology-Driven Solutions: Using advanced tools and apps that monitor contributions and offer personalized advice can empower employees to adjust their strategies in real-time as market conditions change.

The shift from simply getting by to achieving a truly secure retirement demands attention to the often-overlooked subtle parts of planning. It’s about putting aside momentary distractions and focusing on long-term financial health. The current economic situation, riddled with unpredictable market dynamics and rising healthcare demands, calls for a recalibration of priorities—a move from reactive measures to proactive planning.

Conclusion: Embracing a Proactive Approach to Financial Wellness

In today’s unpredictable economic landscape, the puzzle of retirement planning is undeniably challenging. Employees are left to figure a path through a maze of nerve-racking market shifts, inflated healthcare costs, and policy uncertainties. Even as emotional readiness may seem high, the practical steps to ensure that retirement dreams become a reality are too often overlooked.

However, this situation is not without hope. With timely action and collaboration between employees and employers, the current gaps in financial preparedness can be steadily closed. Empowering the workforce with clear guidance, robust benefits, and the right tools is not only key for individual financial security—it is essential for the long-term stability of our entire economy.

Ultimately, the message is clear: the future will be shaped by those who take action today. Whether it’s through setting up detailed written plans, consulting with professional advisers, or embracing technology-driven solutions, every small step is a move toward a more secure retirement. Employers, in particular, have a super important role to play in this journey by fostering a workplace culture that champions financial wellness.

As we continue to witness the evolving picture of retirement preparedness, it is crucial for everyone involved—from workers to policymakers, from employers to financial advisers—to commit to a proactive approach. Now is the time to get into the real work of crafting comprehensive, actionable plans that will ensure our collective future is filled not with worry, but with confidence and stability.

By turning hopeful intentions into concrete strategies, we can bridge the considerable gap between emotional optimism and actual financial readiness. The twists and turns of today’s economic challenges require us all to take the wheel, making informed, decisive moves that ultimately lead to a well-prepared and secure retirement future.

Originally Post From https://www.benefitnews.com/news/iralogix-retirement-readiness-index-shows-savings-gaps

Read more about this topic at

Bridging financial gaps: making banking accessible

Bridging Financial Gaps for Unbanked Residents