Opinion Editorial: Navigating the Tricky Parts of Evolving Trusts, Estates, and Property Law

The legal landscape in the areas of trusts, estates, and property taxation has experienced a whirlwind of changes in 2025 that are both fascinating and, at times, intimidating. As we take a closer look at recent legislative updates and court decisions across various states, it becomes clear that practitioners, fiduciaries, and clients alike must figure a path through a maze of new rules, pending proposals, and judicial interpretations. While the details might sometimes appear off-putting, understanding these updates is super important for anyone engaged in estate planning or fiduciary administration.

In this opinion editorial, we’ll dig into state-by-state developments—from Connecticut’s digital asset clauses to California’s creditor protection reforms—and explore how these legal twists and turns impact planning, administration, and tax exposure. In doing so, we will break down the complicated pieces into manageable insights, with tables, lists, and subtopics to help you steer through the evolving regulatory environment.

Connecticut’s Evolving Estate Planning Landscape

Connecticut Estate Planning Developments 2025

Connecticut has been busy updating its laws surrounding trusts and estates. Recent legislative efforts reflect a clear intent to keep pace with digital trends and changing societal norms.

Key updates include:

- Connecticut Uniform Trust Decanting Act: Effective January 1, 2024, this law permits irrevocable trusts to be decanted, allowing trustees to transfer assets into a new trust with revised terms. This offers flexibility, particularly beneficial when the original terms become misaligned with the settlor’s intent, or when financial needs change in a family.

- Digital Wallet and Virtual Currency Inclusion: With H.B. No. 6990 signed on June 23, 2025, the definition of “property” now explicitly includes digital wallets and virtual currency. This signifies Connecticut’s proactive stance in addressing the modern financial ecosystem.

- Marriage Prohibitions: H.B. No. 6918 prohibits marriage between first cousins. While this update may seem off the central track of estate planning, it demonstrates the state’s effort to align its statutes with evolving social policies.

Furthermore, several pending bills, such as H.B. No. 5333, which would adopt the Uniform Real Property Transfer on Death Act, and proposals to reduce estate tax exemptions or extend filing deadlines, show that the legislative journey in Connecticut is far from over. For professionals advising clients, these updates mean the need to dig into the little details, such as differences in tax thresholds and procedural deadlines.

Managing Tax Implications in Connecticut

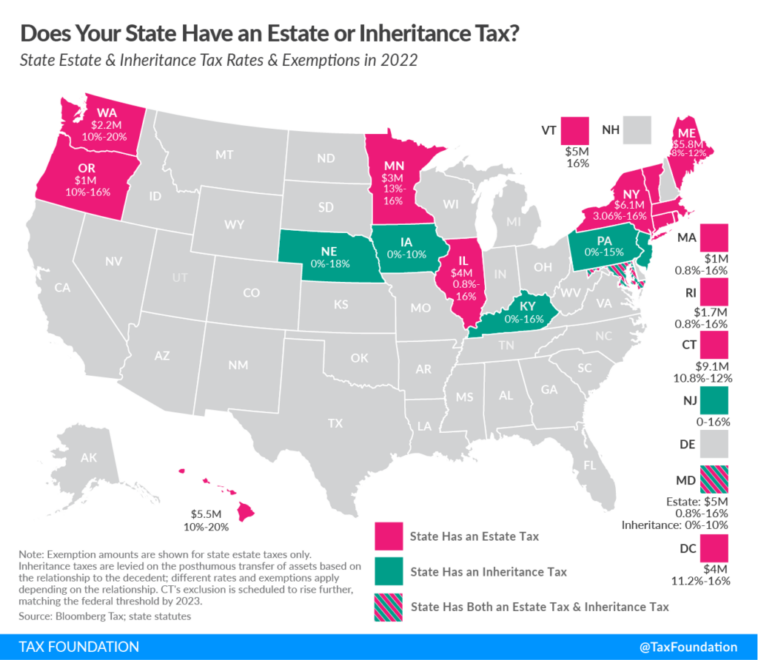

It’s super important to note how Connecticut’s approach to estate and gift tax unification affects estate planning. Residents face state gift tax on all federally taxable gifts, and taxable gifts directly reduce the available estate tax exemption. This calls for a careful weighing of lifetime transfers versus posthumous distributions to ensure optimal tax planning.

A summary table of Connecticut’s key changes follows:

| Legislation | Effective/Status | Key Point |

|---|---|---|

| Uniform Trust Decanting Act | Effective January 1, 2024 | Permits decanting of irrevocable trusts |

| H.B. No. 6990 | Signed June 23, 2025 | Includes digital assets in “property” definition |

| Pending Estate Tax Reforms | Under Consideration | Potential lower exemption thresholds and filing extensions |

By keeping a close eye on these updates, legal advisors can better advise clients on adjusting their estate planning strategies to reduce unexpected tax exposure.

New Jersey: Trusts and Estates in a State of Transition

New Jersey Developments and Court Decisions

Compared to other states, New Jersey experienced relatively few legislative twists and turns in the trusts and estates realm in 2025. However, significant judicial decisions have set important precedents.

One noteworthy case, Archit & Monal Amin v. Director, Division of Taxation, clarified the scope of taxable income concerning undistributed earnings from controlled foreign corporations (CFCs). On New Year’s Eve, the state’s Tax Court unequivocally ruled that state income tax would only apply on dividends when they are actually distributed. This resolution offers some relief from the intimidating prospect of double taxation on undistributed earnings.

Understanding New Jersey’s Inheritance Tax Framework

New Jersey does not impose an estate tax but maintains a state inheritance tax. The approach is nuanced—tax liability depends on whether the decedent was a New Jersey resident, the beneficiary’s relationship to the decedent, and the specific type and value of assets inherited.

Advisors need to figure a path through these subtle details to ensure that estate plans are structured in the most efficient manner possible. Key points include:

- Inheritance tax is imposed on the beneficiary rather than on the decedent’s estate.

- The rate may vary significantly depending on familial relationships and asset types.

- Proper planning is essential to minimize inadvertent tax consequences.

New York’s Push Toward Modernized Estate Procedures

Electronic Execution and Service Reforms in New York

New York is urging a shift towards digital estate planning, introducing several proposals that could transform how wills and other documents are executed and served. A proposed bill, A7856A, has already passed both legislative bodies and awaits the governor’s signature. This bill would enable the electronic execution of wills—an upgrade that could streamline probate proceedings and reduce the nerve-racking delays caused by paper filing systems.

Another pending bill, S8175, intends to adjust the service of process in Surrogate’s Court proceedings. Proposed changes include:

- Allowing service by certified mail without the need for a return receipt.

- Permitting electronic service as an alternative when traditional methods prove challenging.

- Amending service periods both within and outside New York State.

These measures, if put into effect, may fundamentally change the way legal documents are handled and the effectiveness with which beneficiaries receive essential notifications.

Estate Tax Considerations in New York

In New York, estate planning continues to be on edge due to the state’s unique estate tax rules. For decedents, there’s a critical threshold under which no estate tax is applied. However, if the gross estate exceeds 105% of the exemption amount, the benefit is entirely lost. Refinements in planning the distribution of estate assets, particularly through trusts and lifetime gifts, become super important to maximize the tax benefits available under New York law.

Illinois: Reforms in Probate and Fiduciary Administration

Modernizing Probate Procedures in Illinois

Illinois has made several positive strides to simplify the probate process and strengthen the accountability of trustees and fiduciaries. Through legislative reform and appellate decisions, the state is making it easier for modest estates to avoid the lengthy and expensive probate process while setting clear standards for trustees.

Key legislative measures include:

- Small Estate Affidavit Threshold Increase: Effective in early 2026, the threshold has been raised from $100,000 to $150,000. This change excludes motor vehicles from the cap, meaning families dealing primarily with bank and brokerage accounts can settle estates faster and with less expense.

- Expanded Recordkeeping Obligations for Trustees: Trustees are now required to keep a copy of the trust instrument for seven years after termination. They must also perform a reasonable search for assets reported as abandoned for unclaimed property purposes, ensuring they manage all financial twists and turns proactively.

- Revisions to Health Care Decision-Making: Amendments to the Living Will Act and Health Care Surrogate Act clarify the roles of health care agents versus written living wills and advance directives, ensuring that agent decisions take precedence when available. This minimizes the confusing bits in decision-making during critical times.

- Financial Institution Reliance: A new law offers financial institutions protection from liability when relying on court-issued Letters of Office. This development streamlines interactions between institutions and fiduciaries, reducing delays during the critical estate settlement phase.

These changes collectively aim to reduce the tangled issues often associated with probate, making the process smoother for beneficiaries and executors. Legal practitioners in Illinois are encouraged to discuss these updates with clients to adjust estate plans accordingly.

Recent Appellate Decisions that Shape Illinois Trust Law

Illinois courts have recently weighed in with decisions that provide critical guidance on trustee duty and fund distribution. For instance:

- Trustee Duty to Collect Loans: In In re Estate of Sippel, an appellate court clarified that trustees must actively pursue the collection of loans and notes owed to the trust. This decision reinforces the need for trustees to document collection efforts and ensure every dollar owed is recovered.

- Beneficiary Designations Post-Divorce: The Mowen v. Kelly case underlined that divorce does not automatically revoke beneficiary designations on retirement accounts. This ruling affirms that unless explicitly stated in a divorce decree, the original designations will stand despite a marital dissolution.

- Scrivener Exception for Estate Documents: The Roszkowiak v. Roszkowiak decision confirmed that non-lawyers may assist with drafting trust amendments, provided they act only in a ministerial capacity under the direct instruction of the settlor. Such a finding gives parties a bit more leeway in handling routine administrative tasks of trust preparation.

- Standing to Sue Under Power of Attorney: In In re Estate of Piton, the court ruled that only principals or true successors in interest have standing to bring a claim against an agent under the Illinois Power of Attorney Act. This decision significantly narrows the pool of potential litigants, reducing peripheral challenges.

- Disclosure Obligations of Trustees: The Lindblad v. Blair case further refined the trustee’s duty regarding disclosure, specifying that beneficiaries are entitled only to the most recent operative version of a trust instrument unless a validity challenge is raised. This provides much-needed clarity to trustees and beneficiaries about the limits of disclosure rights.

Florida’s Fiduciary and Trust Decanting Modernizations

Fiduciary Income and Principal Allocation Reforms

Florida’s adoption of the Uniform Fiduciary Income and Principal Act (FUFIPA) effective January 1, 2025 introduces a modern approach designed to reflect current portfolio management practices. Essentially, FUFIPA:

- Encourages trustees to apply modern portfolio theory in managing both income and principal.

- Authorizes trustees to make adjustments between income and principal under particular circumstances, offering greater flexibility to balance current income against long-term needs.

- Ensures that, if beneficiaries are damaged by abuses of fiduciary discretion, they are restored to the position they would have occupied otherwise.

This legislative initiative is designed to minimize the nerve-racking delays that can occur when fiduciaries are forced to adhere strictly to outdated accounting guidelines. It could prove particularly useful for beneficiaries dealing with long-term trusts that stand to benefit from a modern approach to asset management.

Enhanced Decanting Capabilities in Florida

Florida has also expanded the flexibility of trust decanting, a process which—as some might say—enables trustees to “pour” the assets of an existing trust into a new structure more in line with current needs or updated tax laws. Key points include:

- Greater Trustee Latitude: Authorized trustees with discretion over principal distributions can now modify trust terms, extend trust duration, and alter beneficiary interests without having to face the grim prospect of litigation.

- Protection for Beneficiaries: While trustees enjoy increased flexibility, the new legislation ensures that beneficiary rights remain substantially similar between the old and new trust structures. This means that family members can avoid unexpected reductions in their beneficial interests.

- Clarification on Limitations Periods: The new law specifies that simply providing notice of intent to decant does not trigger a six-month limitations period. Instead, the clock begins only once the decanting is complete and formal disclosure is made to beneficiaries.

These changes are super important for fiduciaries involved in long-term trusts, as they allow for the adjustment of trust terms without compromising the rights of the beneficiaries. Attorneys should advise clients to plan carefully, ensuring that all documentation meets both the letter and spirit of the law.

Lifetime Gifting and Its Effect on Trust Distributions

A fresh piece of Florida legislation also addresses the potential double benefit that may arise when a settlor makes lifetime gifts to a beneficiary. Under the new statute:

- If the trust instrument expressly states or if a contemporaneous declaration is made at the time of the gift, lifetime transfers may count toward satisfying future trust distributions.

- This measure prevents beneficiaries from enjoying a double windfall—receiving both a lifetime gift and a subsequent trust distribution—thereby preserving fairness in asset allocation.

This update adds another layer of detail to the planning process. Estate planners need to take a closer look at lifetime gifts and carefully document any instructions in writing, ensuring that distributions from a trust remain just and equitable.

Texas: Balancing Property Tax Relief and Business Court Evolution

Key Developments in Texas Tax Legislation

In Texas, where property taxes contribute significantly to the state’s revenue, recent legislative measures have aimed at providing homeowners with some relief while also addressing federal and state taxation issues related to estates.

Notable tax-related developments include:

- Capital Gains on Decedent’s Death: Senate Joint Resolution 18 proposes a constitutional amendment to prohibit capital gains tax on assets transferred at death, a measure that will be on the ballot in November. This could ease the intimidating tax burden on heirs.

- Estate, Gift, and GST Tax Prohibitions: House Joint Resolution 2 aims to lock out any future state-level estate, gift, or generation-skipping transfer taxes, reinforcing Texas’ longstanding stance against such levies.

- Vehicle Gift Tax Adjustments: SB2064, effective September 1, 2025, eliminated certain vehicle gift taxes for decedent estates while maintaining a modest $10 gift tax under defined conditions.

These updates signal the state’s commitment to maintaining a business-friendly tax environment while offering new opportunities for estate planning in Texas.

Property Tax Relief for Texans

Property taxes remain one of the trickiest issues for Texas residents. The state has responded by:

- Offering a homestead exemption that subtracts a portion of the property’s appraised value. In 2025, the available exemption is set at $100,000.

- Proposing constitutional amendments (SB4 and SB23) to raise the homestead exemption further—to $140,000 generally and up to $200,000 for seniors or disabled individuals. The proposed increases could translate to savings of up to $900 for some homeowners.

Below is a simplified table summarizing the current and proposed homestead exemption figures in Texas:

| Category | Current Exemption | Proposed Exemption |

|---|---|---|

| General Homeowners | $100,000 | $140,000 |

| Seniors/Disabled | N/A | $200,000 |

For Texas homeowners, these planned enhancements are essential for lowering property tax burdens. The proposals will be subject to a constitutional vote later this year, so all parties interested in property tax reform should monitor these developments closely.

The Emergence of Texas Business Courts

One of the more intriguing updates in Texas jurisprudence is the formation and implementation of Texas Business Courts. These specialized courts have been designed to handle disputes that involve multi-million-dollar corporate matters, thereby offering a streamlined process for resolving complicated business disagreements.

Some key characteristics of the Texas Business Courts include:

- Jurisdiction over disputes that exceed $5 million, particularly those involving corporate derivative actions and breaches of fiduciary duty.

- Coverage of cases involving publicly traded companies, regardless of the monetary limit in question.

- Consent from the parties for disputes involving contracts or commercial transactions exceeding $10 million.

With nearly 45 opinions issued in just a little over a year, these courts have already begun to influence the legal rights and responsibilities of business owners. For stakeholders considering relocation in a more business-friendly jurisdiction, Texas offers not only favorable tax conditions but also a judicial framework that could simplify the resolution of complex commercial issues.

California’s Reforms: Private Retirement Plans and Creditor Protection

Legislative Adjustments to Private Retirement Plans and Trusts

California continues to lead in the realm of creditor protection, especially when it comes to private retirement plans and trusts. Assembly Bill 2837, effective January 1, 2025, significantly revises the Enforcement of Judgments Law and introduces new measures for the protection of retirement assets.

Some of the key aspects of these reforms include:

- Revised Creditor Protections: The law updates procedures for filing judgments against retirement assets, ensuring that distributions from Private Retirement Plans (PRPs) are better shielded from creditors. This update might be particularly appealing to clients planning for retirement while managing potential liabilities.

- Clarification on Retirement Plan Definitions: Under the California Code of Civil Procedure, courts now analyze a range of factors—such as the debtor’s intent, the timing of the plan’s creation, and the actual use of funds—to determine whether a plan qualifies for protection as a PRP.

- Trust Structures (PRTs): Private Retirement Trusts have firmly established themselves as a key tool for safeguarding retirement assets from creditors. These trusts require structured administration, including annual reviews and independent trustee oversight, to ensure their assets remain secure.

Legal advisors in California are encouraged to work closely with clients on the design and execution of these plans, paying careful attention to the subtle parts of creditor protection laws and regulatory compliance.

Creditor Protection: Then and Now

Before these reforms, retirement assets enjoyed protection by virtue of the Employee Retirement Income Security Act (ERISA) in many instances, though distributions were still vulnerable to certain liens. California’s new approach now requires courts to apply a means test when creditor claims are challenged. Under this test, only the portion of the retirement balance necessary for a retiree’s well-being is protected if a creditor comes after other funds.

Importantly, assets properly held in a PRT remain fully exempt—a strategic move that legal practitioners describe as a game changer for asset protection. These changes are crucial for clients looking to preserve their retirement funds regardless of financial hardships or creditor claims.

Appellate Insights in Trust and Estate Law

Recent appellate decisions in California further illuminate the evolving state of trust administration. Notable cases include:

- Estate of Tarlow: This decision confirmed that trustees of testamentary trusts have standing to petition the probate court for distribution rights. The case has provided clarity on trustee rights under California Probate Code section 11700.

- Packard v. Packard: In this matter, the court held that petitions aimed at reforming a trust—rather than contesting its validity—are not limited by the strict 120-day statute for trust contests. This distinction allows for modifications that reflect the settlor’s true intent without being unduly constrained by procedural deadlines.

These decisions underscore the importance of consulting legal counsel to sort out all the fine shades of trust administration. As practice continues to evolve, attorneys must fully understand each ruling’s implications on both current administration and future estate planning strategies.

North Carolina Updates: Electronic Wills and Paternity Changes

Electronic Storage of Attested Written Wills

North Carolina has taken a significant step forward by embracing digital documentation within estate planning. Under the new law from Session Law 2025-33, attorneys of record now have the option to store original wills in electronic form. This innovation not only streamlines the probate process but also mitigates the nerve-racking challenges associated with lost paper wills.

Key features of the new law include:

- Electronic Record Creation: Only a licensed North Carolina attorney may create an electronic record of the original paper will and then certify a printed copy for use in probate proceedings. This ensures that the transformation from paper to digital is done accurately and securely.

- Revocation Limitations: Once a will has been converted to an electronic record, the testator may not revoke the will through physical destruction, reinforcing the permanence of the act of digitizing the document.

- Effective Date: The law becomes effective on January 1, 2026 and applies to all attested wills stored from that date forward, even if originally executed before the new law came into effect.

This initiative is designed to reduce the complicated pieces of probate litigation that arise from missing or ambiguous documentation. Attorneys and estate planners are advised to educate their clients on these changes and to consider electronic storage as a secure alternative to traditional methods.

Revisiting Paternity Laws in North Carolina

North Carolina’s legal framework regarding paternity has also seen important modifications. Under previous law, a child born to unmarried parents was presumed to be the child of the mother for inheritance purposes. Even if a father’s name appeared on the birth certificate, additional steps were required to establish parental rights.

The revised law, effective December 1, 2025 (for estates of decedents dying thereafter), eliminates the cumbersome requirement of filing an acknowledgment of paternity with the Clerk of Superior Court. This change simplifies the process for establishing a legal parent-child relationship, thereby enabling a clearer path for inheritance rights for children of unmarried parents.

For families and legal practitioners alike, this update removes one of the more intimidating hurdles in paternity claims and helps to avoid potential future disputes over inheritance.

Elective Share and Community Property: Fresh Updates in Estate Distribution

Clarification on Elective Share Requirements

Recent statutory revisions in North Carolina have also impacted the elective share—specifically, how trusts for surviving spouses are valued. Under the updated requirements, a trust must maintain a non-adverse trustee for the entire duration and must explicitly mandate distributions of both income and principal using compulsory language. These provisions ensure that a surviving spouse’s full protection under elective share rules is not inadvertently compromised by discretionary trustee powers.

Legal advisers must take care to incorporate these fine points in drafting estate documents to ensure compliance and protect the surviving spouse’s rights. The detailed requirements include:

- Ensuring that trustee language uses terms such as “shall” or “is required to” to meet the statutory distribution requirements.

- Confirming that all successor trustees are similarly non-adverse, thereby preserving the trust’s status for elective share purposes throughout its life.

Uniform Community Property Disposition at Death Act

Another significant development in North Carolina is the Uniform Community Property Disposition at Death Act. Effective January 1, 2026, the act sets out a fresh framework for handling community property in a state that traditionally follows separate property rules. The law assumes that half of the community property automatically belongs to the surviving spouse, while the other half may be disposed of according to the decedent’s estate plan.

This new framework clarifies several tricky parts about community property transfers and provides time limits for filing claims—usually within one year of a decedent’s death. It also extends protection to third parties acting in good faith, a welcome step in preventing lengthy litigation that could delay estate distributions.

Final Thoughts: Preparing for a Future in Flux

Adapting to the Changing Legal Environment

The evolution of laws governing trusts, estates, and property taxes across multiple states is filled with twists and turns that may seem overwhelming at first glance. However, when we break down these changes into manageable insights, it becomes evident that each update is designed to provide clarity, fairness, and flexibility for both fiduciaries and beneficiaries.

Estate planning professionals, legal practitioners, and clients must work together to update strategies, ensuring that every document reflects the latest legislation and appellate interpretations. Whether you’re dealing with the modernized probate procedures in Illinois, the digital transformation in North Carolina, or the nuanced taxpayer relief measures in Texas, preparation is key.

Key Recommendations for Practitioners and Clients

As a summary, here are some essential steps that advisors and clients should consider:

- Stay Informed: Regularly monitor legislative changes and appellate decisions in relevant states. Staying informed will help you manage your way through these confusing bits and hidden complexities.

- Review Estate Plans: With updates to trust decanting laws, creditor protection measures, and beneficiary designations, it is critical to review and, if necessary, revise existing estate plans.

- Consult Legal Experts: Given the nerve-racking and complex nature of evolving estate and trust laws, collaborating with expert legal counsel remains super important to ensure compliance and protect client interests.

- Embrace Digital Tools: In light of North Carolina’s adoption of electronic storage for attested wills, and New York’s push for electronic wills, adopting digital tools can reduce delays and improve records management.

- Document Thoroughly: From lifetime gifting declarations to trust amendment instructions, ensure that every decision is clearly documented to avoid future disputes. Use clear language and definitive terms such as “shall” to express compulsory obligations.

Looking Ahead with Confidence

The changes unfolding in trusts, estates, and property law are both challenging and full of opportunities. The adjustments we see in Connecticut, New Jersey, New York, Illinois, Florida, Texas, California, and North Carolina all signal a legal environment that is adapting to modern realities—whether through incorporating digital tools, modernizing pension and trust management, or offering enhanced protections for beneficiaries.

For professionals in the field, the critical task is to figure a path through this evolving framework while advising clients on how to best secure their financial futures. The legislative and judicial updates might initially feel intimidating, but with careful planning and thorough attention to detail—paying close attention to every little twist and fine point—they offer significant opportunities to achieve more effective and resilient estate planning solutions.

While the legal horizon is undeniably filled with tangled issues, it is also super important to note that these changes are geared toward creating a more equitable and efficient process for trust administration and estate distribution. Whether you are a legal practitioner, a trustee, or someone planning your legacy, understanding and adapting to these changes can make the difference between a stressful, off-putting experience and a well-organized, secure estate settlement.

Conclusion

As we come to the end of our in-depth exploration of the evolving legal landscape, it is essential to recognize that these changes represent much more than just revisions to archaic statutes. They embody a significant shift toward a more flexible, responsive, and equitable system where the needs of contemporary families, businesses, and individual financial plans are more adequately met.

From Connecticut’s embrace of digital financial definitions to Texas’ innovative business courts and North Carolina’s digital will storage, every development encourages us to take a closer look at how law adapts to our increasingly complex society. Legal professionals must remain vigilant, continually updating their knowledge and strategies to ensure that every client is well-protected against both the nerve-racking uncertainties and the potential benefits offered by new laws.

The road ahead may feature more tangled issues and subtle parts, but with the right guidance, every twist and turn can lead to improved outcomes. As we stand on the cusp of this evolving legal era, let us work together to ensure that our estate planning and trust administration practices are as modern, flexible, and secure as the times demand.

Originally Post From https://www.jdsupra.com/legalnews/state-of-the-states-2025-year-end-3419675/

Read more about this topic at

Reviewing and Updating Your Estate Plan

Modernizing an Outdated Estate Plan – What to do with a …