Preparing Financial Advisors for the Surge in Gray Divorces

In recent years, the increase in “gray divorces”—divorces involving couples aged 65 and older—has been noticeable. As these splits become more common, financial advisors are finding themselves in the unique position of having to rework retirement plans while addressing the many challenging twists and turns brought on by ending a long-term marriage later in life. In our opinion, the role of the financial advisor is evolving, and it is essential to get a closer look at how these changes are reshaping the financial planning process.

Gray divorces bring a number of tricky parts that extend far beyond the simple division of assets. They involve rethinking real estate holdings, tax planning, and insurance coverage, along with the emotional adjustments that accompany ending a lifelong partnership. For advisors, the process is not just about crunching numbers—it also involves understanding the subtle details of each client’s emotional, financial, and legal situation.

Understanding the Current Landscape of Gray Divorces

The divorce rate among seniors is experiencing a notable rise, a phenomenon driven by changing societal attitudes and the evolving nature of personal relationships. With more people choosing to seek separation, advisors are now frequently tasked with helping clients face a future that is full of problems and narratives often riddled with tension.

It is important to recognize that the financial challenges associated with gray divorces are layered. The separation not only disrupts joint financial strategies but also necessitates a complete redesign of retirement planning in many cases. Financial advisors now must find their way through these complicated pieces, ensuring that the new plan meets immediate needs while simultaneously planning for long-term security.

Shifts in Demographic Trends and Their Impact on Financial Planning

One of the most critical drivers behind the rise in gray divorces is the shifting demographic landscape. As life expectancies increase, many seniors find themselves with decades of retirement ahead of them. This longevity, combined with a more progressive view of individual happiness and personal fulfillment, has contributed to the growing acceptance of divorce later in life.

Older individuals now have more opportunities to start over and reinvent themselves, no longer restrained by societal expectations that once kept couples together despite underlying issues. Advisors must now work with clients who are not only reorganizing their financial lives but are also reimagining their futures. The need to replan retirement funds, adjust spending habits, and even reconsider long-standing housing arrangements means that every decision carries a myriad of subtle details and hidden complexities.

Challenges and Opportunities for Advisors in Gray Divorce Cases

The challenges faced by financial advisors in these scenarios are both extensive and nerve-racking. The advisor’s task goes well beyond simple money management—they must also help clients figure a path through their emotional upheavals and the reallocation of shared liabilities. Below is a list summarizing some of the key areas where advisors have to be particularly mindful:

- Retirement Savings Reallocation: Splitting retirement funds and adjusting contributions for individual survival.

- Real Estate Decisions: Determining whether to sell a shared home, buy new property, or adjust property portfolios.

- Tax Considerations: Addressing the tax implications of dividing assets and changing filing statuses.

- Insurance Adjustments: Updating life and health insurance policies to reflect new risk profiles and beneficiary changes.

- Estate Planning: Revising wills, trusts, and beneficiary designations to reflect the new reality.

Each of these categories comes with its own set of complicated pieces and fine points that require specialized expertise. The stakes are high, and the advisor must be ready to steer through these issues with both financial savvy and sensitivity.

Building a Comprehensive Strategy for Replanning Retirement

When working with older clients facing divorce, financial advisors must develop strategies that consider a wide spectrum of financial components. The task involves digging into each aspect of a client’s portfolio to ensure that every factor is addressed, from short-term liquidity needs to long-term growth objectives. Crafting a successful plan involves several critical steps:

Conducting a Thorough Financial Audit

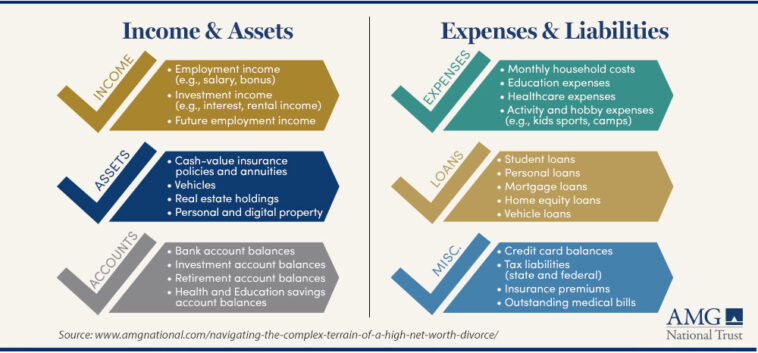

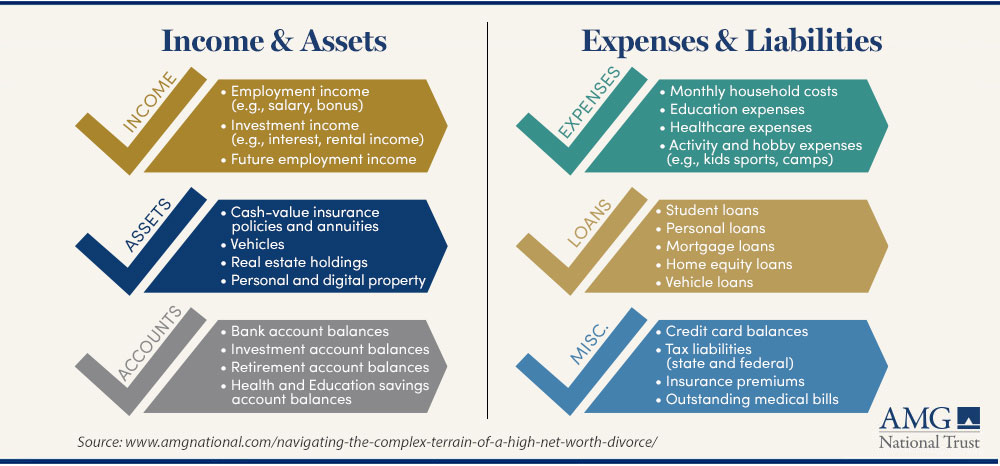

One of the first steps for any advisor is to perform a complete audit of the client’s finances. This audit serves as the baseline measurement, helping identify all incomes, liabilities, and assets that need to be redistributed or restructured. The process is detailed and full of small distinctions that can make or break the overall strategy. It includes:

- Analyzing retirement accounts and pension plans.

- Reviewing investment portfolios and asset allocations.

- Assessing current debts and liabilities, including mortgages.

- Evaluating insurance policies to determine their suitability.

- Scrutinizing estate documents to ensure they reflect current wishes.

During this phase, the advisor’s role is to sort out the layered issues one by one, paying close attention to even the least obvious details. This careful examination is essential for developing a sound, post-divorce financial plan that will carry the client comfortably into their later years.

Developing a New Budget and Financial Forecast

Once the complete audit is finished, the next stage is to work on a realistic and tailored budget that meets the new financial realities. Older adults, particularly those approaching retirement, may face dramatic shifts in income. It is both critical and super important to craft a financial forecast that encapsulates anticipated changes, potential risks, and emerging opportunities.

This process involves:

- Identifying fixed expenses such as living costs, healthcare, and daily necessities.

- Projecting changes in income streams, particularly those reliant on joint income sources that might now become individual responsibilities.

- Estimating the potential need for long-term care or unforeseen expenditures.

Advisors must also build in a buffer for emergencies and unplanned events. The budget should not only reflect current realities but be agile enough to adapt to new developments as they arise. A comprehensive forecast can empower clients to feel more in control, even when the future seems loaded with issues.

Introducing a Multi-Pronged Investment Approach

Post-divorce financial planning for seniors often requires a reimagined investment strategy. Given the nearing of retirement, many clients find themselves confronted with the need to balance risk and security more cautiously. Advisors, therefore, are tasked with constructing an investment portfolio that mitigates risks while allowing for moderate growth.

A typical approach might include:

- A mix of fixed-income securities to provide stable income streams.

- Consideration of dividend-paying stocks for periodic payouts.

- Incorporation of low-risk mutual funds or exchange-traded funds (ETFs) that fit a rebalanced portfolio model.

- Potential real estate investments that offer steady rental income.

This multi-faceted investment strategy must be constantly revisited and adjusted as the client’s circumstances change. Every decision made along the journey must be weighed against how it fits into the broader financial picture, ensuring that it complements other components of the retirement plan while addressing the subtle details inherent in post-divorce life.

Understanding Property Division and Real Estate Considerations

For many older couples, the family home is one of the most substantial assets. Deciding whether to keep, sell, or buy new property is often one of the most nerve-racking and complicated pieces for advisors and their clients. Real estate decisions in gray divorces are rarely straightforward, as they bring with them both financial and sentimental value.

Assessing the Value of Shared Real Estate

The process of property division involves digging into the exact value of the home and related property. This appraisal must be meticulous, as it not only helps in splitting assets equitably but also affects subsequent financial planning. Factors involved include:

- Current market conditions and property appraisals.

- Outstanding mortgage balances and potential refinancing issues.

- The potential impact of selling the property on future living arrangements and mobility.

Often, the property is not just a financial asset—it carries deep personal and familial significance. This dual nature means the advisor must work through both the solid numerical value and the small shades of emotion attached to the property. The goal is to help clients find a balanced approach that safeguards their financial interests without disregarding sentimental attachments.

Legal and Tax Implications of Property Division

Rethinking property matters following a divorce opens up a range of legal and tax-related challenges. It is essential to coordinate closely with legal professionals to take into account the following:

- Potential capital gains tax implications when selling property.

- Changes in property tax assessments due to a shift in ownership.

- The need to rework estate plans to ensure that revised property holdings are legally protected.

Advisors need to work with both legal and tax experts to ensure that every small twist in the property division process is managed efficiently. The aim is to avoid any unexpected financial pitfalls and to secure the adjusted property assets in a responsible manner that benefits the client over the long run.

Tax Management in the Post-Divorce Landscape

Tax considerations are always a critical part of financial planning, but for seniors undergoing divorce, these issues become even more compelling. From filing status changes to asset transfers, the tax implications of a gray divorce are numerous and can often be intimidating. Financial advisors play a key role in ensuring that their clients are well-prepared and informed about the tax burdens they may face.

Key Tax Considerations for Divorcing Seniors

When seniors split, the tax situation might change drastically. The advisor must help clients puzzle out the new tax liability by focusing on the following aspects:

- Revising tax filing status from joint to individual, which can affect overall tax liabilities.

- Understanding the tax consequences of dividing retirement accounts and other investments.

- Assessing potential deductions related to legal fees and other transitional expenses.

- Planning for the future, including potential tax liabilities when liquidating or transferring assets.

With these elements in mind, a detailed tax plan should be created in coordination with a tax specialist. Memorably, every small distinction in tax law could influence the final financial picture. The advisor’s role is to help clients sort out these taxing issues, ensuring that every step taken minimizes unnecessary burdens and leverages available credits and deductions.

Coordinating with Tax Professionals

No financial advisor works in a vacuum, especially in the realm of post-divorce planning for seniors. It is off-putting to handle the entire process alone. Bringing in tax experts not only alleviates the pressure but also provides nuanced insights into how the divorce will impact future tax obligations.

Key benefits of this coordinated approach include:

- Clarifying the new structure of income taxation following divorce.

- Addressing any potential audits or compliance issues that might arise.

- Identifying tax-efficient strategies for asset division and transfers.

Partnering with tax professionals creates a safety net that enhances the overall financial planning strategy. Clients benefit from a comprehensive plan that respects each small twist in tax law while ensuring efficiency and compliance in the aftermath of divorce.

Reworking Insurance Policies and Protecting Future Stability

Divorce can dramatically alter a senior client’s risk profile—both personally and financially. Insurance products must be revisited, and policies updated to reflect the new circumstance. This necessity is yet another example of the many tangled issues that advisors face in gray divorces.

Shifting Insurance Needs Post-Divorce

The breakdown of a long-term marriage means that policies that were once joint may no longer be appropriate. Both parties may need to secure their own coverage for various types of insurance, including:

- Life insurance, to ensure dependents and beneficiaries are clearly defined.

- Health insurance, which might be affected by retirement status or other changes in employment and benefits.

- Long-term care insurance, a vital consideration for seniors planning a secure future.

Advisors are tasked with finding and comparing policies that are both competitively priced and tailored to the client’s unique risk profile. The insurance market is loaded with subtle details that might affect coverage rates, deductibles, and overall premiums. Thus, it is essential to carefully sort through these options and guide clients toward products that offer stability and peace of mind.

Implementing a Customized Insurance Strategy

Given the significant impact that insurance policies can have on a senior’s financial health, advisors should take a methodical approach to update or replace outmoded insurance policies. This process can involve:

- Reviewing existing policies and identifying any gaps in coverage.

- Comparing quotes from multiple providers to ensure competitive rates.

- Evaluating the need for bundled policies that can lower costs and streamline management.

- Continuously assessing whether new life circumstances require further adjustments down the line.

With careful consideration of these small twists and hidden complexities, advisors can ensure that clients remain protected against unforeseen future risks. This carefully orchestrated insurance strategy is not only crucial for mitigating future uncertainties but also instrumental in constructing a comprehensive financial plan that addresses every aspect of post-divorce life.

Estate Planning and Wealth Transfer Considerations

Estate planning is another area that requires significant rethinking after a gray divorce. For couples who have built their lives and accumulated wealth together, the separation mandates a complete reworking of wills, trusts, and beneficiary designations. This part of the financial puzzle is filled with subtle details and fine points that, if overlooked, could have long-lasting implications.

Revising Wills, Trusts, and Beneficiaries

The divorce necessitates an immediate review of all estate planning documents. Advisors must help their clients take a closer look at the following critical issues:

- Updating beneficiary designations on retirement accounts, life insurance policies, and investment portfolios.

- Revising wills to ensure that assets are distributed according to the new intentions of the client.

- Modifying trusts to reflect the changed family dynamics and to avoid any potential conflicts later on.

This process is particularly nerve-racking because it deals with matters that extend far beyond immediate financial concerns. The fine details of estate planning are super important, as they safeguard your legacy and ensure that your wealth is transferred according to your wishes. For many, the emotional weight of these decisions can be as significant as the financial considerations.

Strategies for a Smooth Wealth Transfer

Ensuring the smooth transfer of wealth in the aftermath of a divorce requires a well-thought-out strategy. Financial advisors often recommend a step-by-step plan that may include:

- Meeting with estate planning attorneys to review existing documents.

- Scheduling regular reviews—ideally, annually—to accommodate any changes in personal or financial circumstances.

- Establishing clear guidelines for how assets should be separated and reallocated over time.

For seniors, engaging in this process early can help ease the transition and provide much-needed assurance during an otherwise tense time. Advisors must help clients work through these decisions, ensuring that every small twist is addressed with sensitivity and expertise.

Emotional and Psychological Considerations in Financial Replanning

It is impossible to discuss gray divorces without mentioning the emotional impact that accompanies such life-altering decisions. In many cases, financial planning is closely intertwined with personal identity, family history, and future aspirations. Advisors need to be mindful of the fact that each client is also grappling with emotional upheaval.

Addressing the Emotional Aspects Head-On

While financial decisions are based on numbers and projections, the underlying emotions can heavily influence a client’s choices. Advisors can help by:

- Providing clear, transparent explanations to ease clients’ fears about the future.

- Encouraging clients to engage with professional counselors or therapists as they adjust to their new circumstances.

- Recognizing that sometimes, decisions made in the heat of emotional distress may need to be revisited with a clearer perspective later on.

This holistic approach, which addresses both financial and personal concerns, enables advisors to build trust and long-term relationships with their clients. By acknowledging and working through the emotional hurdles as clients replan their retirement and financial future, advisors deliver a service that goes far beyond simple asset management.

Creating a Supportive Network

One of the best strategies to help clients manage the challenges of gray divorce is to create a network of support. This network might include:

- Legal professionals specializing in family law and divorce.

- Tax experts who can simplify the nuanced twists of new taxation resulting from the divorce.

- Mental health professionals who understand the nerve-racking nature of such life changes.

- Peer support groups where clients can share experiences and coping strategies.

With a robust support system in place, clients are better equipped to take charge of the many small parts of their new financial reality. The support network not only addresses the complicated pieces of divorce but also provides encouragement, ensuring that clients feel less intimidated by the future that lies ahead.

Innovative Tools and Technology in Post-Divorce Planning

As financial landscapes become more dynamic, innovative tools and digital technologies are increasingly playing a pivotal role in post-divorce planning. From retirement planning applications to real-time analytics on asset performance, these tools help identify hidden complexities and guide clients through the various small distinctions in their new portfolios.

Digital Platforms for Comprehensive Financial Analysis

Today’s technology offers solutions that enable advisors to provide more detailed and personalized advice than ever before. Digital financial planning platforms can help in:

- Tracking and forecasting financial performance under various scenarios.

- Simulating different asset division strategies to identify the optimal split.

- Highlighting potential risks with advanced analytics that break down how small twists may impact overall wealth.

These platforms not only offer a more transparent view of all elements of a client’s portfolio but also allow for quick adjustments as new information comes to light. With the technical support provided by these tools, the seemingly overwhelming process of replanning becomes more manageable for both advisors and clients.

Enhancing Client Communication and Understanding

Innovative software and interactive dashboards are also proving super important in bridging the communication gap between advisors and clients. The benefits include:

- Clear visualizations that simplify complex financial data into understandable charts and tables.

- Real-time updates that help clients monitor the performance of their investments.

- Automated alerts and recommendations that guide appropriate adjustments to the financial plan.

By integrating these technological solutions, advisors can make the entire process feel less intimidating. Clients gain better insight into every subtle detail of their financial plan, which in turn builds confidence and encourages informed decision-making as they transition through their new phase of life.

Case Studies and Practical Examples for Gray Divorce Financial Planning

To further illustrate the multi-faceted challenges and opportunities involved in gray divorces, it is useful to consider a few case studies and scenarios that demonstrate effective strategies. These real-world examples shed light on the process, offering valuable lessons for both financial advisors and clients.

Case Study 1: Splitting Retirement Accounts and Restructuring Investments

Consider the case of a retired couple who had jointly invested in a diversified portfolio of stocks, bonds, and real estate assets. Facing a gray divorce, the couple needed to separate their assets while ensuring that each party was financially secure for the remainder of their retirement. The advisor in this case:

- Performed a detailed audit of all retirement accounts and investments.

- Created individualized plans that redistributed investments to account for varying risk tolerances.

- Coordinated closely with tax professionals to minimize negative tax consequences on any asset liquidations.

This approach ensured that both parties ended up with balanced portfolios that met their individual needs, demonstrating how financial planning can be adapted to manage the subtle details associated with asset division.

Case Study 2: Revising Real Estate Holdings and Creating a New Budget

Another example comes from a scenario where one partner owned the family home, a major asset that needed to be evaluated for its market potential as part of the divorce settlement. The advisor in this scenario:

- Assisted in obtaining an up-to-date appraisal of the property.

- Developed a plan that outlined the pros and cons of selling versus keeping the property.

- Integrated the decision into a reworked overall budget that considered potential changes in living arrangements and future maintenance costs.

The attention paid to even the smallest twisting turns in the property strategy allowed the client to make a well-informed decision, aligning the final resolution with long-term financial stability.

Practical Tips for Financial Advisors Working with Gray Divorce Clients

Given the range of dynamic issues described above, financial advisors who are working with seniors undergoing divorce may benefit from several practical tips. These guidelines ensure that advisors are ready to figure a path through each of the many complicated pieces.

Establish a Clear, Step-by-Step Process

An organized approach can make the overall process feel less overwhelming. Advisors should consider establishing a step-by-step framework that includes:

- Initial comprehensive financial reviews and assessments.

- Prioritizing immediate vs. long-term financial needs.

- Coordinating with legal, tax, and mental health professionals as necessary.

- Creating a timeline for the reevaluation of strategies as client circumstances evolve.

This structured process not only builds client trust but also creates a clear roadmap for managing every twist and turn encountered during the transition.

Maintain Open and Consistent Communication

Communication is key when dealing with situations that are as emotionally charged as gray divorces. Advisors must:

- Schedule frequent check-ins to monitor client satisfaction and adjust strategies as needed.

- Provide clear explanations for every decision, breaking down the fine points of each action in a way that is easy to understand.

- Create detailed but accessible financial reports, supported by tables or charts when necessary, to illustrate progress and performance.

This open dialogue allows clients to feel more in control of their financial destiny, reducing anxiety and ensuring that even seemingly nerve-racking decisions are made with confidence.

Stay Abreast of Regulatory Changes and Market Trends

The legal and financial landscape is continuously evolving, and advisors need to be well-informed about new regulations, market trends, and emerging financial instruments. By staying current with industry changes, advisors can:

- Advise clients on the potential impact of regulatory updates on their asset structure.

- Integrate new investment avenues and digital tools that can improve the overall planning approach.

- Provide proactive recommendations that preemptively address future financial twists.

This vigilant approach to the latest developments is essential, as it ensures that the planning strategy remains robust and capable of withstanding any unforeseen changes.

The Future of Financial Planning in an Era of Gray Divorce

Looking ahead, the trend of gray divorces is likely to continue as societal norms evolve and people live longer, more active lives. Financial advisors will need to be even more agile, combining empathy with strategic financial guidance to help clients transition smoothly into this new phase of life.

In the future, it is expected that advisors will increasingly rely on technology, continuous education, and collaborative networks to manage the re-planning process effectively. As the financial sector adapts to the emerging needs of senior clients, there will be a stronger emphasis on personalized services that address each individual’s unique combination of financial, legal, and emotional challenges.

Preparing for Long-Term Challenges

The long-term outlook requires a proactive mindset. Advisors must think beyond immediate concerns and prepare strategies that remain resilient in the face of evolving economic conditions and regulatory frameworks. This preparation includes:

- Regularly updating financial plans to incorporate new legislation and market dynamics.

- Leveraging advanced digital tools that offer real-time monitoring of financial health.

- Building interdisciplinary teams that include legal, tax, and insurance experts.

By integrating these practices into daily operations, financial advisors can continue to provide comprehensive advice that makes sense of all the tricky parts and hidden complexities that gray divorces present.

Embracing a New Era of Financial Advisory Services

This evolving landscape presents a unique opportunity for financial advisors to redefine their roles, moving away from mere number crunchers to become trusted partners in clients’ life journeys. As advisors take the wheel in reworking retirement plans, they not only assist with asset management but also play a critical role in ensuring that seniors enjoy a secure, fulfilling future.

In conclusion, gray divorces require a thoughtful, detailed, and pliable approach to financial planning. By paying attention to every small twist—from taxation and asset division to insurance adjustments and estate planning—advisors can help their clients transition into the post-divorce phase with confidence. While the process is undoubtedly intimidating and loaded with issues, a well-planned, collaborative strategy can iron out the nerve-racking details and guide clients to a stable, secure future. The future of financial planning in this context is not only about managing money but also about reimagining life after divorce with dignity and foresight.

Final Thoughts

Financial advisors who are equipped to work through the many complicated pieces of gray divorce will ultimately provide their clients with a roadmap that is both clear and adaptable. The mixture of emotional support, legal guidance, tax expertise, and robust technological tools creates a powerful network of support that helps seniors confidently launch into their next chapter. For advisors embracing this challenge, every effort to take a closer look at each hidden complexity transforms the daunting into the doable, paving the way for a more secure and vibrant retirement.

As the prevalence of gray divorces continues to rise, so too will the demand for financial advisors who can figure a path amidst the confusing bits and overlapping issues intrinsic to these separations. In meeting this demand, advisors not only safeguard their clients’ financial well-being but also redefine the standard of care in a field that is ever-changing, ensuring that every client receives guidance that is as nuanced and individualized as the life they continue to build beyond divorce.

Originally Post From https://www.financialadvisoriq.com/c/4940504/679844

Read more about this topic at

Gray Divorce After 30 Years: A Guide to Peaceful Separation

How to Navigate the Legal Hurdles of Gray Divorce – Law